An overview of our sell-side M&A services

What History Tells Us About the AI Transition in SaaS

Over the past several months, a growing number of articles, including several in the Wall Street Journal – have focused on artificial intelligence and what it means for the software industry.

At the center of the debate is a question:

If AI changes the economics of software, what happens to the companies that benefited from the old economics?

For founders, investors, and acquirers, this conversation moves beyond product capabilities and into something more fundamental. AI not only changes the competitive dynamics of software markets, it also changes how buyers evaluate durability, pricing power, retention, and long-term value.

That does not mean the SaaS model is broken. Or that existing software companies are suddenly irrelevant.

But the market is already reassessing many of the assumptions that historically supported software valuations.

How AI is Rewriting the Economics of Software

The current debate around AI is ultimately a debate about durability.

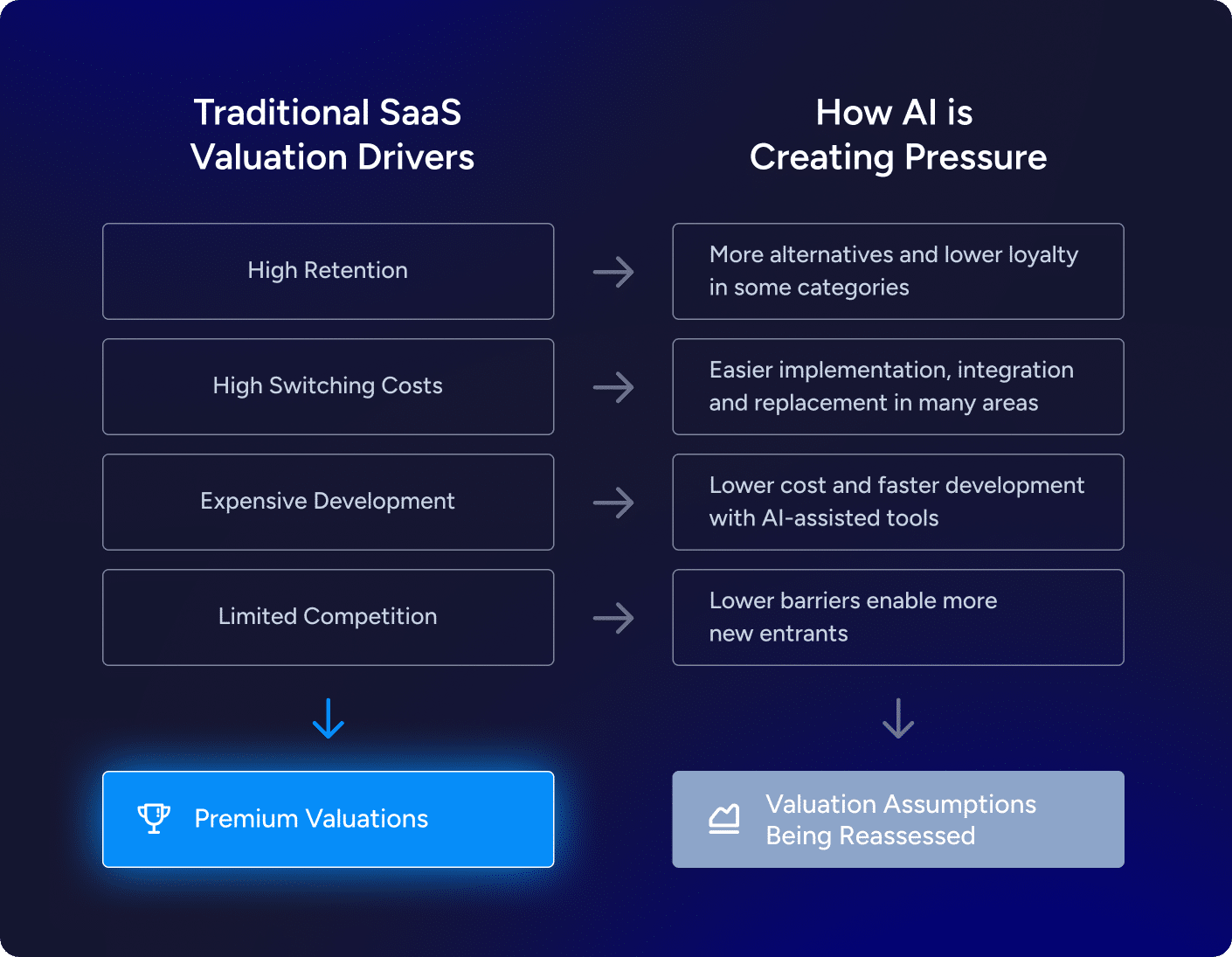

For years, software valuations benefited from a set of assumptions investors viewed as relatively stable: Recurring revenue was sustainable, switching costs were meaningful, development was expensive, and established companies had structural advantages that protected retention and pricing power.

AI is putting pressure on those assumptions. Let’s take a look at a few.

Gross Revenue Retention

Retention has long been one of the clearest indicators of software quality and revenue durability. Companies with strong retention historically received premium valuations because their future cash flows are viewed as more predictable and less risky.

AI is changing the dynamics that supported those assumptions. Barriers to building competitive products are falling in certain categories, product cycles are compressing, and customers have more alternatives than they did just a few years ago.

That is changing pricing power and customer expectations. And in some markets, it’s changing retention dynamics. The result is that buyers are starting to look more carefully at how durable recurring revenue is.

Switching Costs

Many software businesses historically benefited from the operational difficulty of replacing embedded systems. AI reduces some of that friction. As implementation, integration, and customization become easier, customers become more willing to evaluate alternatives. In categories where products become increasingly comparable, switching behavior changes.

That does not eliminate switching costs entirely. But it does weaken one of the structural advantages many software companies have relied on for years.

Build vs. Buy

AI is also changing the economics of software development itself.

Internal teams can build applications faster and at a fraction of the historical cost. Tasks that once required large engineering organizations increasingly can be handled by much smaller teams supported by AI tools. As development costs fall, some of the advantages SaaS vendors have historically held narrow.

That is changing the build-vs.-buy conversation across the industry.

Why the Outcome is More Nuanced Than It Appears

At the same time, software markets rarely reset overnight.

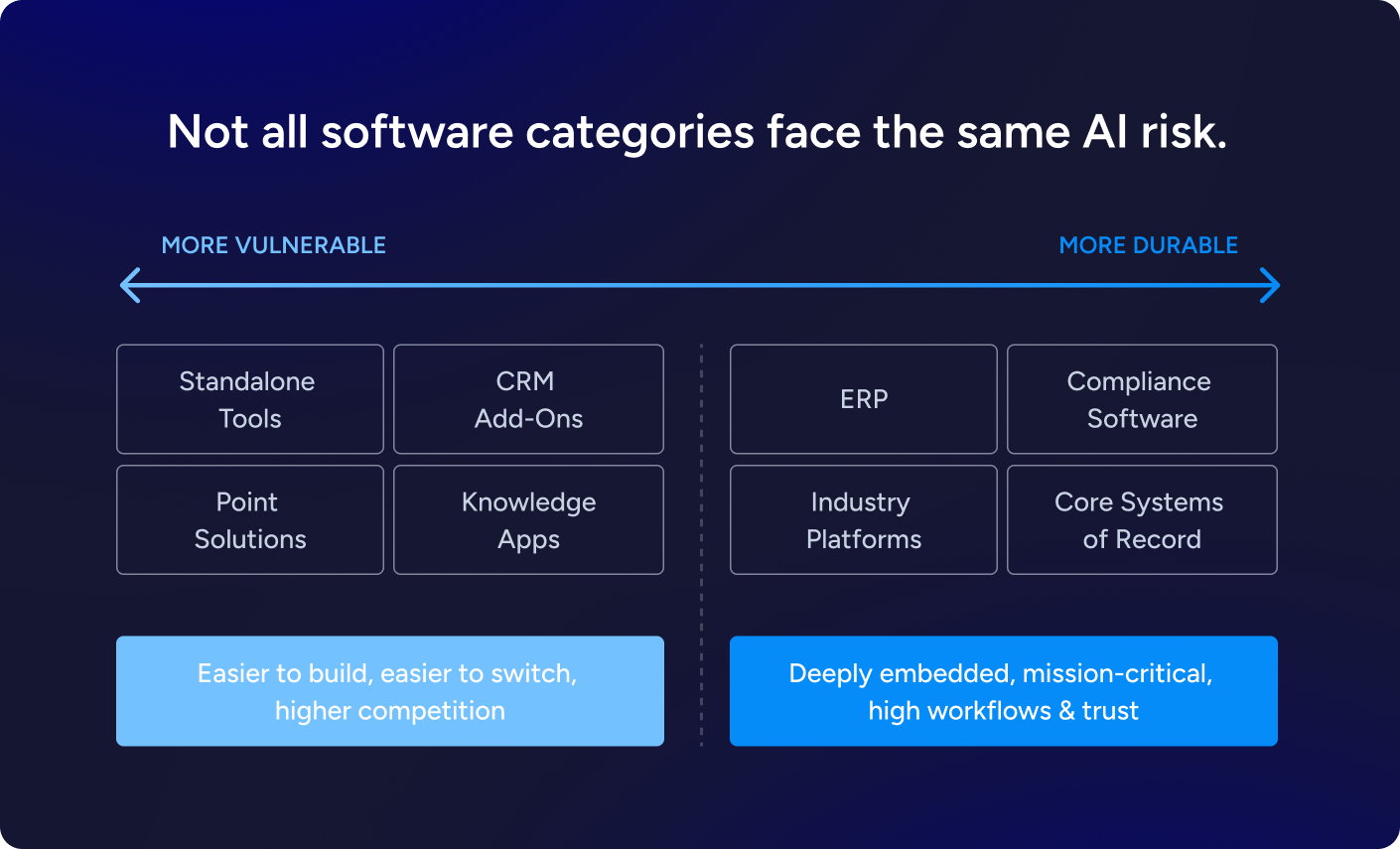

AI is lowering barriers in parts of the software industry. But software products are not evaluated solely on functionality. They are embedded in workflows, integrated across broader systems, and supported by years of operational knowledge, implementation work, and customer relationships.

For example, retention has always been influenced by far more than product features alone. Switching costs, workflow disruption, implementation complexity, compliance requirements, vendor trust, customer support, and organizational inertia all affect customer behavior. Companies that deliver value and maintain strong customer relationships are not suddenly becoming vulnerable simply because software development is becoming faster.

The same dynamic applies to the build-vs.-buy debate.

Companies attempted to build internal software platforms long before AI-assisted development existed. Some succeeded, but many did not. Here’s why: SaaS vendors build products for hundreds or thousands of customers at the same time. Product roadmaps evolve through broad market feedback, ongoing investment, and years of operational experience.

Internal development teams, on the other hand, typically build for one company. Even if AI makes development easier, it doesn’t eliminate the complexity of maintaining, securing, scaling, and continuously improving software over time.

AI reduces friction in many areas of software development and implementation. But reducing friction is not the same as eliminating it entirely. Embedded systems, operational dependencies, customer trust, and long-standing workflows still create advantages for many SaaS vendors.

As a result, the impact of AI is unlikely to be uniform across the software industry. Some categories are already experiencing pricing pressure and heightened competition. Others remain relatively insulated. In many cases, competitive dynamics are adjusting without impairing the durability of the underlying business.

Why This Debate Feels Familiar

One of the more interesting aspects of today’s AI discussion is how closely it resembles earlier transitions in software history.

During the transition from on-premise software to SaaS 20 years ago, many observers believed incumbent software vendors would struggle to survive the shift. At the time, most enterprise software companies operated on perpetual license models built around large upfront payments and maintenance contracts.

The argument was that these companies were too tied to their existing economics and operating structures to successfully adapt.

The pressure was real. Moving from perpetual licenses to subscriptions squeezed short-term revenue and cash flow. Sales organizations built around large upfront contracts had to change their compensation structures. Product teams had to move to continuous delivery models. Support organizations had to manage hosted infrastructure.

Many concluded that SaaS-native companies would inevitably displace incumbents across the industry.

Some did. Some incumbents moved too slowly and lost relevance. Others failed to adapt altogether.

But many established software companies rebuilt their products, redesigned their business models, retrained their organizations, and navigated the transition far more effectively than the market initially expected.

The transition was disruptive, but it was not uniformly fatal.

What History Suggests Happens Next

Technology transitions rarely affect every company equally.

During the shift from on-premise software to SaaS, the companies that adapted most successfully were generally those willing to rethink their products, operating models, and go-to-market strategies early on. The companies that struggled most were often those that underestimated the speed and significance of the transition until competitive pressure had already reached its peak.

That same pattern is already emerging during the AI transition.

Some software companies are moving aggressively, integrating AI into their products, improving efficiency, accelerating development cycles, and strengthening their competitive positioning.

Others are moving too slowly.

Every major technology transition reallocates value across an industry.

In some categories, increased competition is placing pressure on pricing and retention. At the same time, lower development and operating costs are improving margins, accelerating product development, and creating meaningful operating leverage.

That matters because software valuations are not driven solely by growth rates. They are driven by the relationship between growth, durability, risk, and cash flow generation.

If AI helps strong software companies operate more efficiently while maintaining long-term customer relationships, some businesses may benefit from stronger economics than they had before.

What’s Different This Time

Despite the historical parallels, there is one major difference between the AI transition and prior software transitions: speed.

The shift from on-premise software to SaaS unfolded over more than a decade. Companies had time to redesign products, retrain teams, restructure operations, and adapt business models over multiple market cycles.

The AI transition shrinks that timeline.

Development cycles and product iteration are accelerating. Customer expectations are changing in real time, and new competitors can emerge almost overnight.

That creates enormous pressure on companies that historically relied on slower product cycles, entrenched market positions, or operational inertia. SaaS companies do not have 10 years to figure this out.

What Separates Winners from Losers

Ultimately, the AI transition is becoming less about the technology itself and more about organizational adaptability.

The SaaS transition did not eliminate on-premise providers overnight. Many struggled, some missed the shift entirely, but many others evolved. They rebuilt their products, changed their operating models, and ultimately prevailed.

Many of today’s SaaS companies will do the same. That said, what took a decade during the shift to SaaS may unfold over just a few years in the age of AI.

The companies navigating this period successfully are staying close to their customers, moving quickly, and rethinking long-standing assumptions about product development, pricing, operations, and organizational structure.

Others are struggling because their companies are moving too slowly.

For founders, this transition is personal. Technology shifts require energy, experimentation, and a willingness to continuously evolve. Not every founder wants to rebuild products, restructure teams, rethink pricing models, and navigate another major platform transition.

Some founders will embrace that challenge. Others won’t.

The software industry has experienced disruptive transitions before. AI will create winners and losers just as prior platform shifts did. The strongest will be the ones that adapt fastest while preserving the customer relationships and operational advantages that made their software businesses valuable in the first place.