An overview of our sell-side M&A services

How Strategic and Financial Buyers Differ in Software M&A

The assumption that strategic buyers pay more and private equity buyers extract more has shaped how many founders think about their options before a process begins.

In practice, buyer behavior is shaped far more by underwriting assumptions, portfolio context, and how a specific business fits into a larger strategy than by the labels. The category a buyer belongs to tells you something. It rarely tells you enough.

What drives behavior, how a deal gets structured, what gets prioritized in diligence, what the business looks like two years after close – sits underneath the label, not on top of it.

Understanding that distinction matters for anyone trying to read a process clearly.

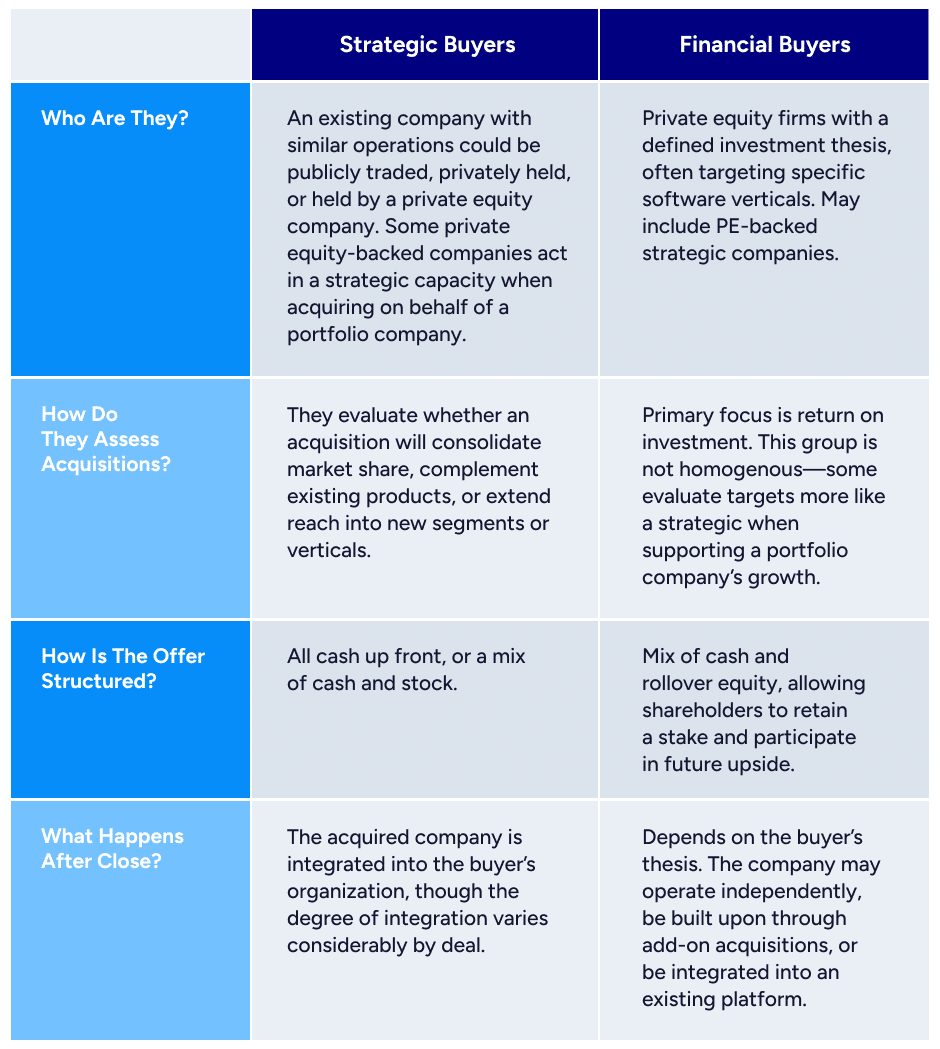

Strategic vs. Financial Buyers: A Quick Reference

How Strategic Buyers Evaluate Software Businesses

Strategic buyers typically pursue acquisitions to accelerate something they cannot build quickly enough internally. They could be publicly traded, privately held, or held by a private equity company.

Because they already operate at scale, they tend to evaluate targets through the lens of fit and speed. Common motivations include market expansion into new customer segments or geographies, product integration that fills a roadmap gap, cross-selling opportunities across an existing customer base, and competitive positioning, including acquisitions intended to protect their core business from a specific threat.

When the strategic rationale is strong, buyers may be willing to pay a premium. That said, the assumption that strategic buyers reliably pay higher multiples than financial buyers is less reliable than it once was. Today, valuation depends more on how well a buyer’s specific value drivers align with the target’s metrics than on buyer type alone.

Strategic buyers tend to prefer straightforward structures when integration risk is low and the rationale is clear. Where there is more uncertainty, particularly around product integration or growth assumptions, earnouts and milestone-based components are more common.

What happens after a strategic acquisition?

Strategic buyers do not follow a single integration playbook. In some cases, the acquired company is kept largely intact and operated as a standalone unit. In others, integration runs deeper across teams, systems, and operations. Every deal reflects the specific reasons the acquisition was made, and the integration plan should protect what made the business worth acquiring.

A common misconception is that synergies always involve headcount reductions at the acquired company. In practice, many strategic buyers keep the target team intact and find efficiencies elsewhere, sometimes within their own organization rather than the seller’s. It’s important to note that every strategic acquisition has a different underlying thesis. Some acquisitions may be defensive. Some may be to acquire customers, some may be to acquire a full business unit to keep in tact.

How Financial Buyers Evaluate Software Businesses

Private equity buyers typically have a defined investment thesis and a clear view of the sector or vertical they are targeting. They approach acquisitions with a three-to-seven-year horizon and a plan for value creation during that period.

Many are more growth-oriented than founders expect. They actively reinvest in sales, product development, and infrastructure. Like strategic buyers, they evaluate many of the same fundamentals: customer retention, product strength, and the growth trajectory of the industry. The analytical frame is similar. The underlying goal is different.

Financial buyers more commonly use structures that include rollover equity and performance-based incentives. This allows founders to retain a stake and participate in future value creation. The structure reflects a partnership orientation rather than a clean handoff.

How Financial Buyers Behave After Close

Private equity buyers are frequently a natural fit for founders who want to stay involved in leadership after close, want a partner to help professionalize operations and build infrastructure for scale, and want to retain equity and participate in the business’s next chapter. That orientation shows up in how these buyers structure deals and how they operate post-close.

John Halloran, founder of Mobile Health, had built a SaaS solution he believed could make healthcare more accessible and affordable. He knew the business needed a larger platform to reach its potential, but he was direct about his concern: he did not want to step away and watch the business go sideways. Working through a structured process, he ultimately partnered with H.I.G. Growth Partners. What followed reflected how a PE buyer with a clear thesis tends to operate: they provided the growth infrastructure the business needed, preserved Halloran’s leadership role, and maintained the operational continuity that made the business worth acquiring. The structure was a consequence of how H.I.G. underwrote the deal, not an accommodation made after the fact.

What happens after a financial acquisition?

The path depends on why the buyer invested. Is the business a platform investment, intended to serve as a foundation for add-on acquisitions? Or is it an add-on to an existing portfolio company?

Some financial buyers retain the business’s independence and focus on organic growth. Others pursue a buy-and-build strategy, acquiring complementary businesses to build out a broader platform. For founders who want a second opportunity to participate in that upside, rollover equity structures make that possible.

For a look at which private equity firms are most active in software M&A right now, see Who’s Driving Software M&A: 10 Private Equity Firms to Know.

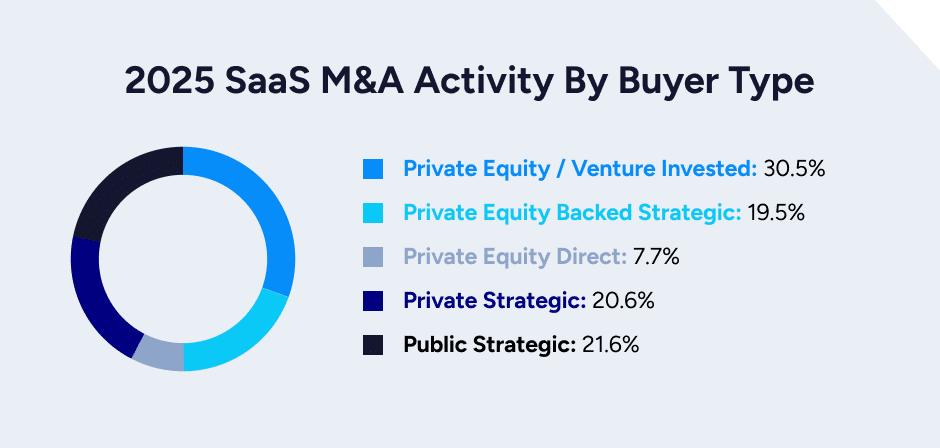

What the Buyer Landscape Looks Like

Strategic and financial buyers are not cleanly separable categories. Many strategic buyers are backed by private equity. Some financial sponsors operate platform businesses that behave more like strategics in practice. The lines are porous.

According to SEG’s 2025 Annual M&A data, activity broke down as follows:

The distribution reflects a market where the buyer universe is broader than the standard two-category framing suggests. For any given business, the relevant question is less about which type of buyer to approach and more about which buyers’ growth objectives align with the business itself.

That question is worth sitting with before a process begins. Founders are often surprised to find that the buyer type they initially expected to be the right fit is not the one most aligned with what they want from a transaction.

Understanding how buyers behave in a process is more useful than tracking the category. The labels are a starting point. What lies beneath them shapes outcomes.

About the Author

Daniel Bowen brings a decade of buy-side M&A experience to his work representing software founders at SEG. Before joining the firm, he served as Vice President of Corporate Development at RealPage, where he developed an acquisition strategy and managed more than 30 strategic acquisitions and integrations across Real Estate.

That experience on the other side of the table shaped how Daniel works with founders today. He spent years reviewing CIMs, sitting across from advisors in management meetings, and watching how deals came together or fell apart. He now applies that perspective to help sellers understand what buyers are evaluating and what preparation looks like from both sides.