An overview of our sell-side M&A services

What Buyer Data Reveals About the Software M&A Market

If you’re a software, SaaS, or AI founder thinking about a transaction, buyer behavior matters. Who’s active, what they’re buying, and where capital is being deployed all shape the environment a process runs in.

What the data does not do is tell you when to sell or what your company is worth. That’s where buyer data gets misread. SEG’s Annual SaaS M&A Report aren’t meant to predict outcomes. It‘s meant to give founders a baseline for how the market is behaving: who’s leaning in, who’s pulling back, and where attention is building.

They’re meant to give founders a baseline for how the market is behaving: who’s leaning in, who’s pulling back, and where attention is building.

Why Software Buyer Data Matters

Most founders want to know: Is now a good time to sell?

When deal volume ticks up or headlines say buyers are active again, it’s easy to assume the market will do the work for you. In reality, that’s rarely how deals play out.

Buyer data is useful because it helps answer a few practical questions:

- Is demand expanding or contracting?

- Are strategic buyers or private equity firms driving activity?

- Which sectors are attracting real attention right now?

What it does not do is tell you how your process will unfold. Market reports look backward by definition. Buyer sentiment shifts faster than quarterly numbers can capture. Trying to time an exit based on reports alone usually leads to frustration.

Used properly, however, buyer data creates situational awareness. It helps you understand the environment you’re operating in before you layer in the things that determine outcomes: retention, growth durability, positioning, and buyer fit.

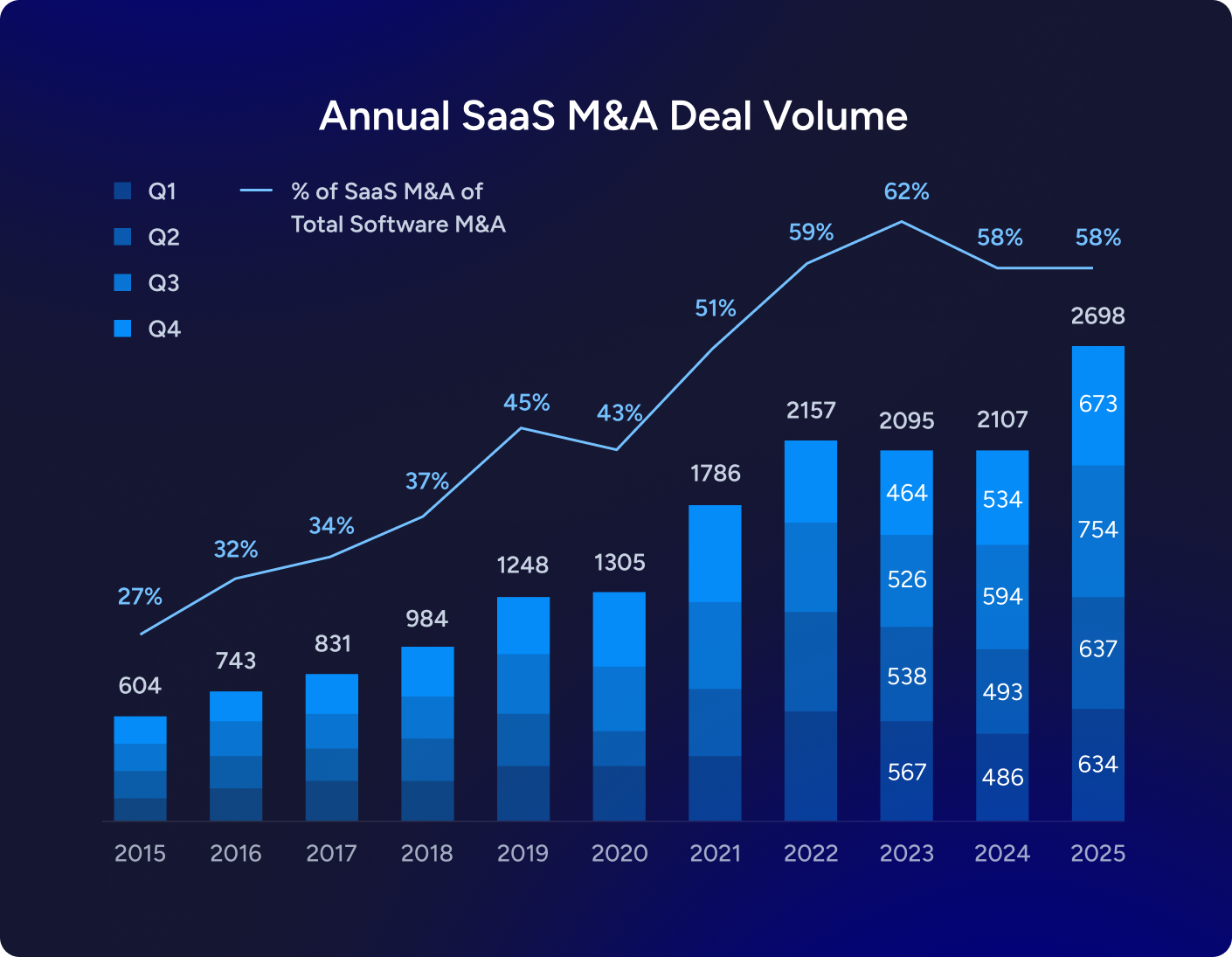

What the 2025 Deal Volume Shows

At a high level, SaaS M&A activity remains strong, with high-quality assets demanding higher valuations. Quarterly deal counts and year-to-date volume provide a snapshot of market momentum. Comparing those figures to prior quarters and the same period last year helps show whether activity is building, holding, or cooling.

For founders, this answers a simple question: Is capital still moving?

In most quarters, the answer is yes. But not evenly, and not for everyone. Activity levels shape competition and process dynamics. They don’t guarantee outcomes.

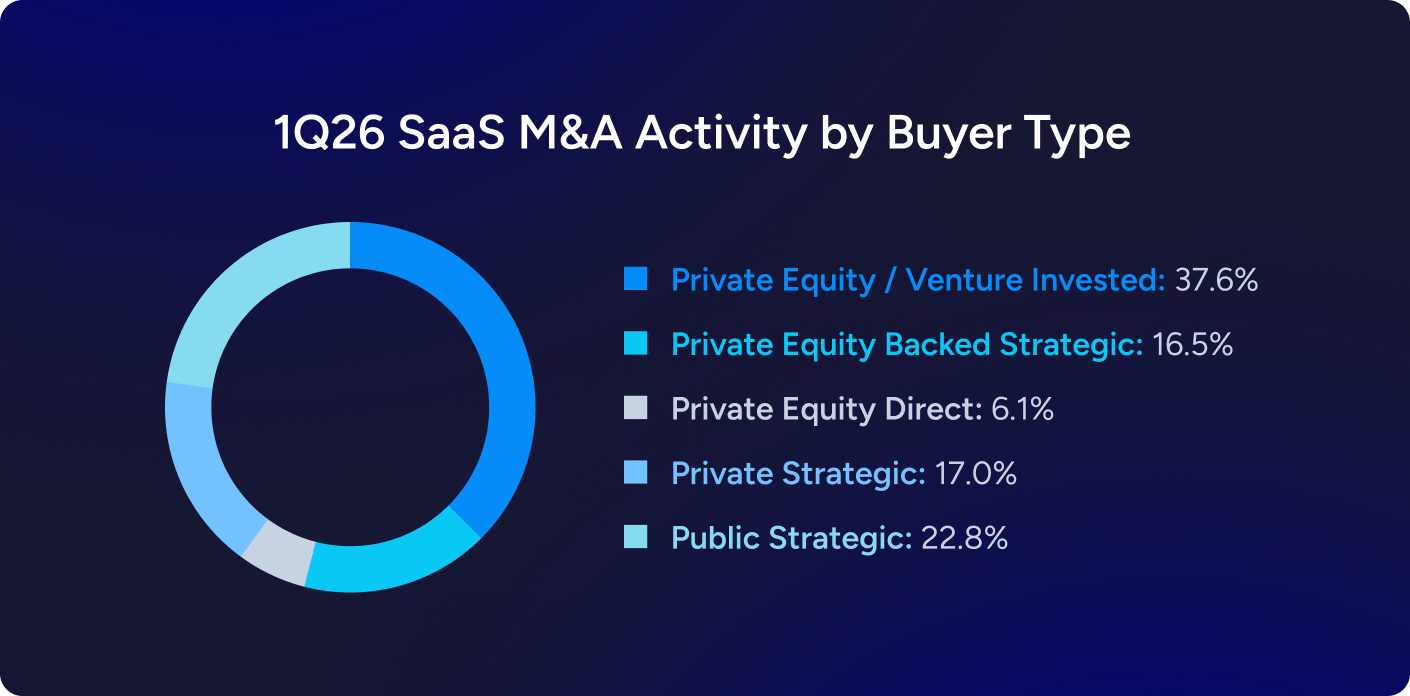

Strategic vs. Private Equity Buyers: Who’s Driving SaaS M&A?

Founders often ask whether strategic buyers or private equity firms are “driving” the market.

But these groups are not opposites. Private equity is not one buyer type. Growth investors, control-focused sponsors, platform builders, and add-on specialists all underwrite risk differently. Strategic buyers are not automatically cost-cutters either. Some acquisitions preserve teams and operate independently. Others are built around synergies that change the organization.

The more useful question is which group is more active. It is determining which buyer profile fits a specific business, its metrics, its market position, and its trajectory.

Private equity and venture-backed buyers remain highly active in SaaS M&A, participating in 60% of all transactions in 1Q26. However, private equity direct investments accounted for only 6.1% of deals and have trended lower over the last few quarters, suggesting greater restraint in new platform formation.

By contrast, PE / venture-invested buyers reached more than a third of SaaS deal activity, while public strategics stayed active at close to a quarter of deals. Together, those trends point to a market increasingly driven by add-ons and strategically motivated acquisitions rather than new platform creation.

Read more: How to Select the Right Buyer for Your SaaS Company’s Next Chapter

Where Buyer Demand Is Growing

Buyer activity varies by sector, and it always has. Some verticals consistently attract attention because they sit at the center of regulated, mission-critical workflows. Others heat up around technology shifts or consolidation cycles, then cool off.

Vertical SaaS has accounted for more than 50% of total SaaS M&A in recent quarters, underscoring investor demand as buyers prioritize resilient high-value companies in essential industries.

In the SEG’s latest quarterly report, Healthcare and Financial Services topped the list of top 10 verticals by percentage of deals.

Tracking deal volume by sector helps founders benchmark where they sit relative to the market. Crowded sectors can create seller competition just as easily as buyer competition. Quieter sectors can still transact well when fundamentals stand out. Sector momentum provides context. Buyers still underwrite individual business fundamentals.

Biggest Buyer Moves This Quarter: What to Pay Attention To

Headline deals are most useful when you look past the headlines. Strategic acquisitions can indicate consolidation or market entry. Private equity platform investments often reveal where sponsors see long-term expansion opportunities. If you’d like to review the most recent software deals by vertical or product category, you can visit the SEG SaaS M&A Deal Database™.

The more useful questions to ask when reading headline activity:

- Are buyers building platforms or filling capability gaps?

- Are deals expanding geography, product scope, or customer base?

- Are buyers paying for scale, defensibility, or future optionality?

Those patterns tell you more about buyer intent than valuation alone.

For a closer look at which buyers are most active and what they’ve acquired, visit Top Strategic Buyers and Top Private Equity Firms.

The Key Shifts Changing Software M&A

Founders benefit from watching direction over time, not reacting to isolated data points. Comparing activity across quarters and year-over-year separates structural shifts from short-term noise. Changes in sector activity, buyer mix, or deal size that repeat tend to reflect shifts in priorities.

In the 1Q26, SaaS M&A hit a record high with 659 transactions, up 24% YoY. Smaller, product-focused acquisitions drove healthy volume but lower average deal sizes. The momentum reflects continued demand for quality SaaS assets.

What one quarter does not tell you is whether the next quarter will match it. Direction matters more than any single data point.

What Buyer Data Can and Cannot Tell You

Market data describes the environment. It does not determine outcomes within it.

Founders who use buyer trends well tend to treat them as one input among several. Rising activity signals that capital is moving, and buyers are engaged. Sector concentration signals where competition for assets is building. Buyer mix signals which underwriting frameworks are most prevalent. None of that tells a founder whether their business is ready, what it will be valued at, or how a specific process will unfold

The businesses that transact well in any market share a common characteristic: their fundamentals hold up when a buyer looks closely. Buyer data can help a founder understand the environment. What happens inside a process is determined by the business itself.

Download your copy of the latest SaaS M&A and Public Market Report.

About Daniel Bowen

Daniel Bowen spent a decade on the buy side before joining SEG, including time as Vice President of Corporate Development at RealPage, where he led acquisition strategy and managed more than 30 transactions. In that role, he was on the receiving end of the market data founders now read in quarterly reports. He saw firsthand how buyer activity translated into actual deal behavior, which sectors attracted serious capital, and where the gap between market signals and individual outcomes was widest.