An overview of our sell-side M&A services

Software M&A by Product Category: 2025 Full-Year Review | SEG

SaaS M&A hit a record in volume of transactions in 2025, with 2,698 transactions globally, a 28% increase year over year. This number only tells you one thing: The market was active.

But it doesn’t tell you where buyers were focused, what they were acquiring, or how deal characteristics varied across categories.

These questions matter for anyone trying to understand the software market today.

One way that we slice SaaS M&A data is by product category, focusing on what a company offers rather than the industry it serves. SEG tracks deal activity across eight product categories, and each tells a different story.

What follows is a view of SaaS M&A by category in 2025, including what buyers acquired, who was most active, and where patterns point. The analysis is based on SEG’s full-year transaction data for North American targets.

The Big Picture: How to Read the 2025 Market

The most useful overall view of the market is how activity was concentrated by category, buyer type, and by what buyers were prioritizing.

Activity concentrated around data, workflows, and revenue systems.

Three categories led the market:

- Analytics & Data Management

- Content & Workflow Management

- Sales & Marketing

The first two together alone accounted for roughly 32% of total SaaS deal activity for the year. These sit at the center of how businesses operate.

Deal activity was consistent throughout the year for these three categories; no single quarter drove volume up. Sustained volume points to durable demand, not opportunistic buying tied to short-term conditions.

Private equity drove volume; strategic buyers drovecompetitive intensity.

Private equity firms were highly active across every category, participating as platform investors or financial backers of add-on acquisitions. Buyers with any strategic angle, regardless of backing, comprised about 92% of all transactions, underscoring that strategic outcomes are driving most M&A volume. Strategic buyers were more selective, but also more aggressive where they showed up. Their activity concentrated in Sales & Marketing and Financial Applications, where established platforms acquired capabilities they couldn’t afford to build slowly.

AI was everywhere, but not equally valued.

About 72% of SaaS M&A targets referenced AI in 2025. That number reflects how widely AI language has spread, not how many companies have meaningful AI differentiation. Buyers are making that distinction, according to SEG’s State of AI in SaaS survey. The companies attracting the most attention are positioned in the infrastructure and workflows where AI operates, not those simply marketing it.

Related: The AI Reset – How SaaS Founders Can Reinvent, Defend, or Exit Stronger

Volume and value didn’t show up in the same places.

Categories like Business Management and Human Capital Management generated the highest deal counts outside of the top three. Meanwhile, Financial Applications, Supply Chain Management, and Asset & Facilities Management produced some of the largest individual transactions of the year.The category-level view shows how these dynamics varied across different parts of the market.

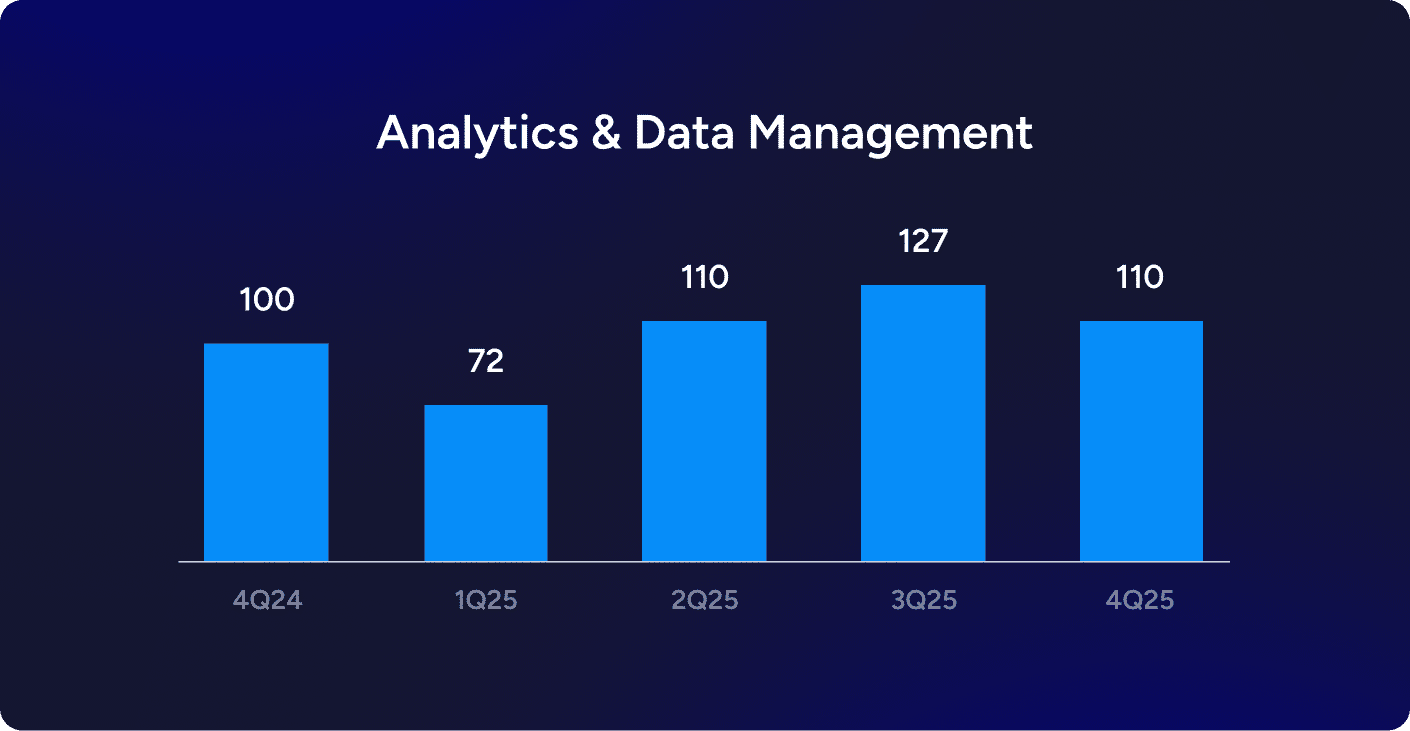

1. Analytics & Data Management

Core finding: Buyers are consolidating the data layer behind AI.

419 deals | Most active category | Only category with expanding public multiples YoY (+11%)

Analytics & Data Management was the most active category in 2025 and the only one where public median EV/TTM multiples expanded, rising 13% year over year.

When deal volume and valuations increase at the same time, it points to sustained buyer conviction.

The transactions illustrate this: IBM’s $11 billion acquisition of Confluent, and Salesforce’s $8.8 billion acquisition of Informatica were about owning the infrastructure that connects, governs, and activates data. That’s what makes AI investments produce usable outputs.

Across the category, buyers focused on platforms that sit at the center of data architecture:

- Snowflake expanded into governance and virtualization

- ServiceNow and Atlassian acquired data-catalog and governance platforms

- Fivetran continued consolidating the data transformation pipeline

The pattern holds across verticals. Healthcare deals centered on clinical analytics and revenue cycle optimization. Financial services deals focused on data integration and investment intelligence. In energy, Blackstone’s take-private of Enverus reinforced the value of domain-specific data platforms.

These companies are embedded in how data moves across systems. As AI becomes more dependent on clean, connected data, that position becomes harder to displace.

In 4Q2025, median EV/TTM multiple was 4.5x in Analytics & Data Management.

What this tells us: Buyers are prioritizing control of the data layer that sits under AI, not just the applications built on top of it.

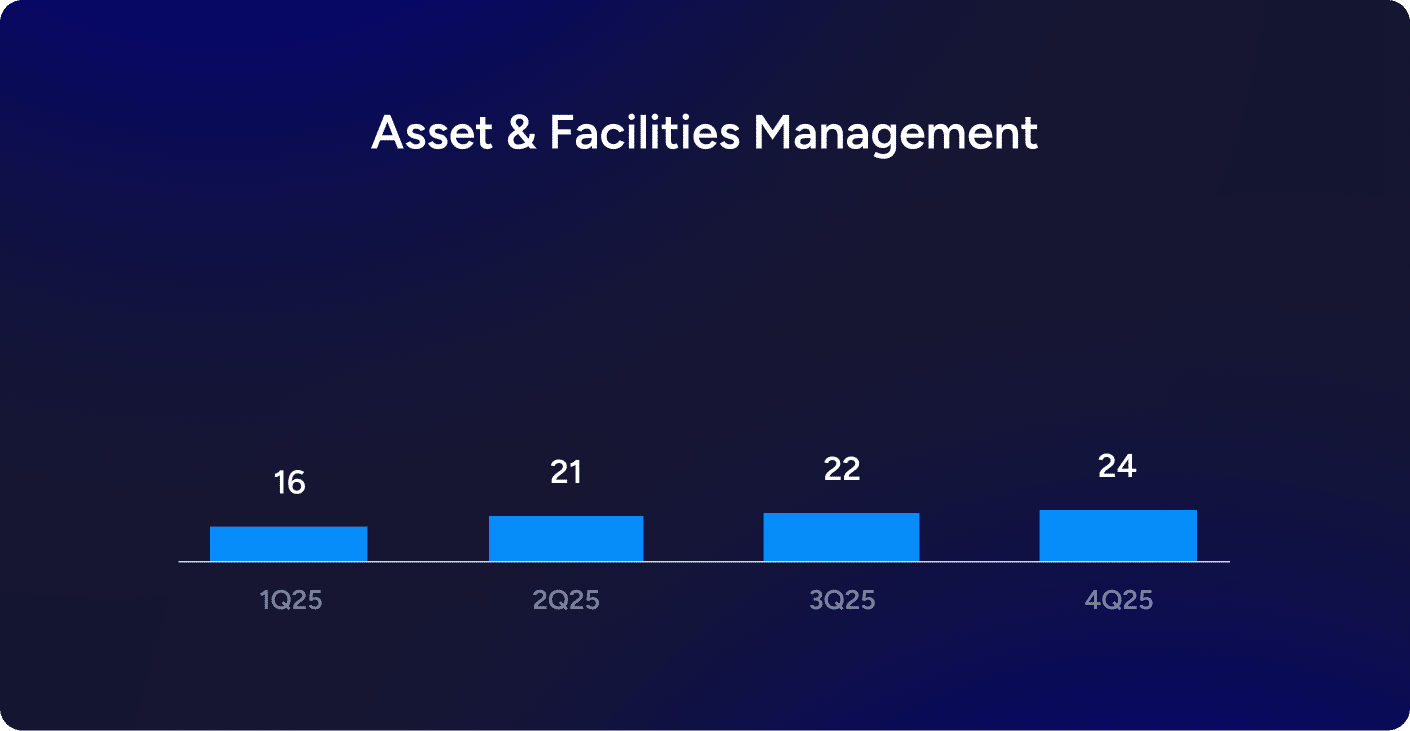

2. Asset & Facilities Management

Core finding: Buyers are prioritizing operationally embedded software with durable retention.

83 deals | Highest PE concentration (69.8%) | Fleet software consolidation across all four quarters

This category is defined by software that is embedded in the physical world: managing fleets, infrastructure, equipment, and facilities.

Once these systems are integrated into daily operations they are difficult to replace, which makes them a target for buyers focused on durable cash flow and long-term value creation. Activity spanned multiple verticals, including transportation, automotive, and real estate, with buyers assembling broader platforms from specialized solutions such as compliance, predictive maintenance, EV fleet management, and IoT-based tracking.

Energy infrastructure also emerged as a key area of focus in the second half of the year. Itron’s $525 million acquisition of LocusView and TPG’s acquisition of Irth Solutions highlight growing demand for software that can manage complex utility and pipeline infrastructure. As grid modernization accelerates, these platforms are becoming more central to operations.

Manufacturing execution systems followed the same pattern; these platforms connect directly to shop-floor operations and production workflows, making them highly embedded and difficult to displace once implemented.

The common thread across all of these: operational dependency.

What this tells us: Buyers are prioritizing software that sits inside physical workflows, where integration and real-world operations create stickiness and defensible value.

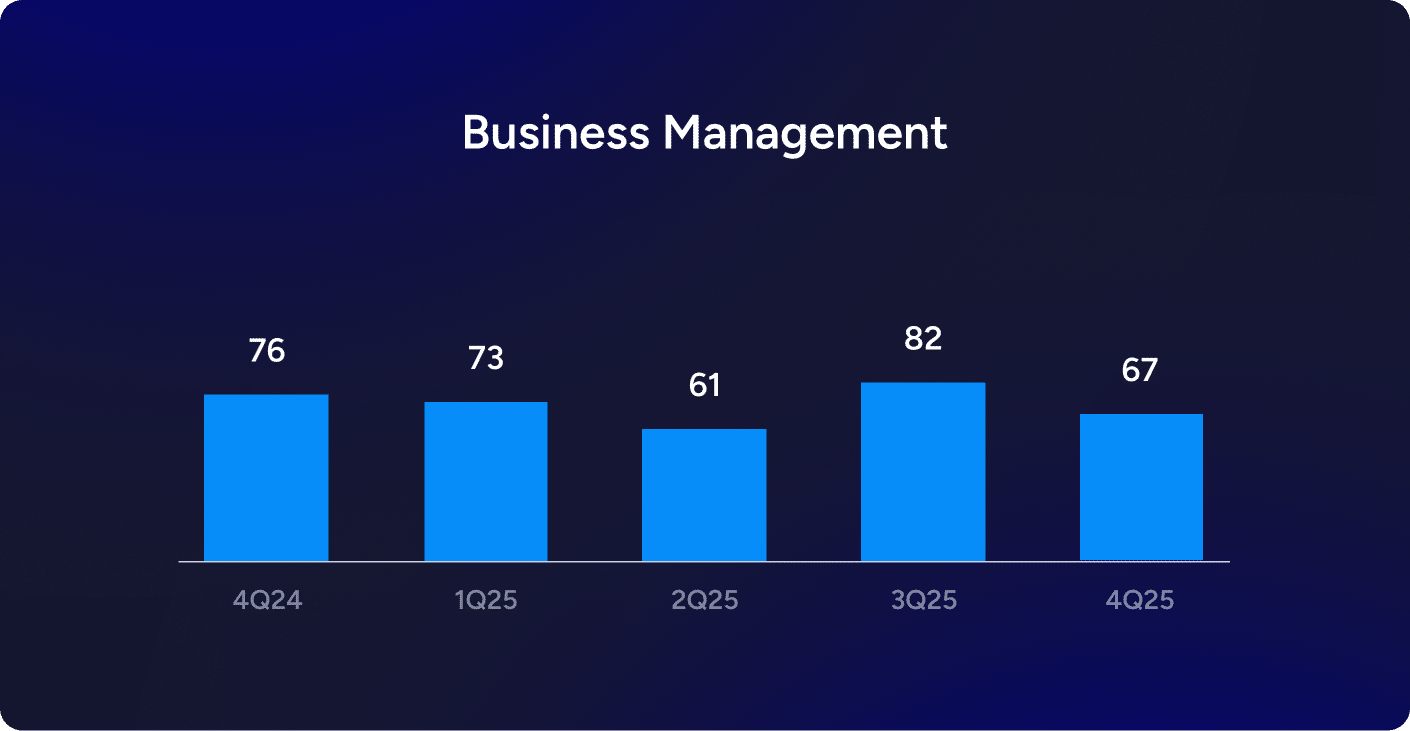

3. Business Management

Core finding: Buyers are acquiring vertical operating systems with high built-in switching costs.

283 deals | Five transactions above $1B | Take-private activity signal strongest in this category

Business Management was one of the most active categories in 2025, but what stood out wasn’t volume alone. It was what buyers were targeting. Buyers consistently sought out platforms built for specific industries, including roofing contractors, restaurants, fire departments, retirement-plan providers, and others. These applications are attractive because they serve as systems of record. They manage core workflows, customer interactions, and day-to-day processes that businesses rely on to function. As a result, they become deeply embedded in customer operations, create high switching costs, and carry value that buyers are willing to pay for.

Aptean’s $2.35 billion acquisition of AccuLynx VLEX (manufacturing) and Thoma Bravo’s take-private of Olo (restaurant) reflect this. These platforms are deeply embedded in customer operations, and replacing them would require rebuilding how the business functions.

Take-private activity was concentrated in this category, with multiple transactions above $1 billion. That includes NEC’s $2.8 billion acquisition of CSG Systems, Patient Square Capital’s $2.7 billion take-private of Premier, and Vista Equity’s $2 billion acquisition of Acumatica. That shows that these buyers believe public markets are undervaluing the durability of these businesses, particularly their retention and long-term cash flow potential.

Verticals reinforced the trend. Healthcare produced the highest deal count, while government and public safety platforms also attracted investment, including JMI Equity’s minority investment in First Due.

What this tells us: Buyers are prioritizing vertical-specific platforms that function as operating systems for their customers, where deep workflow integration creates durable retention and long-term value.

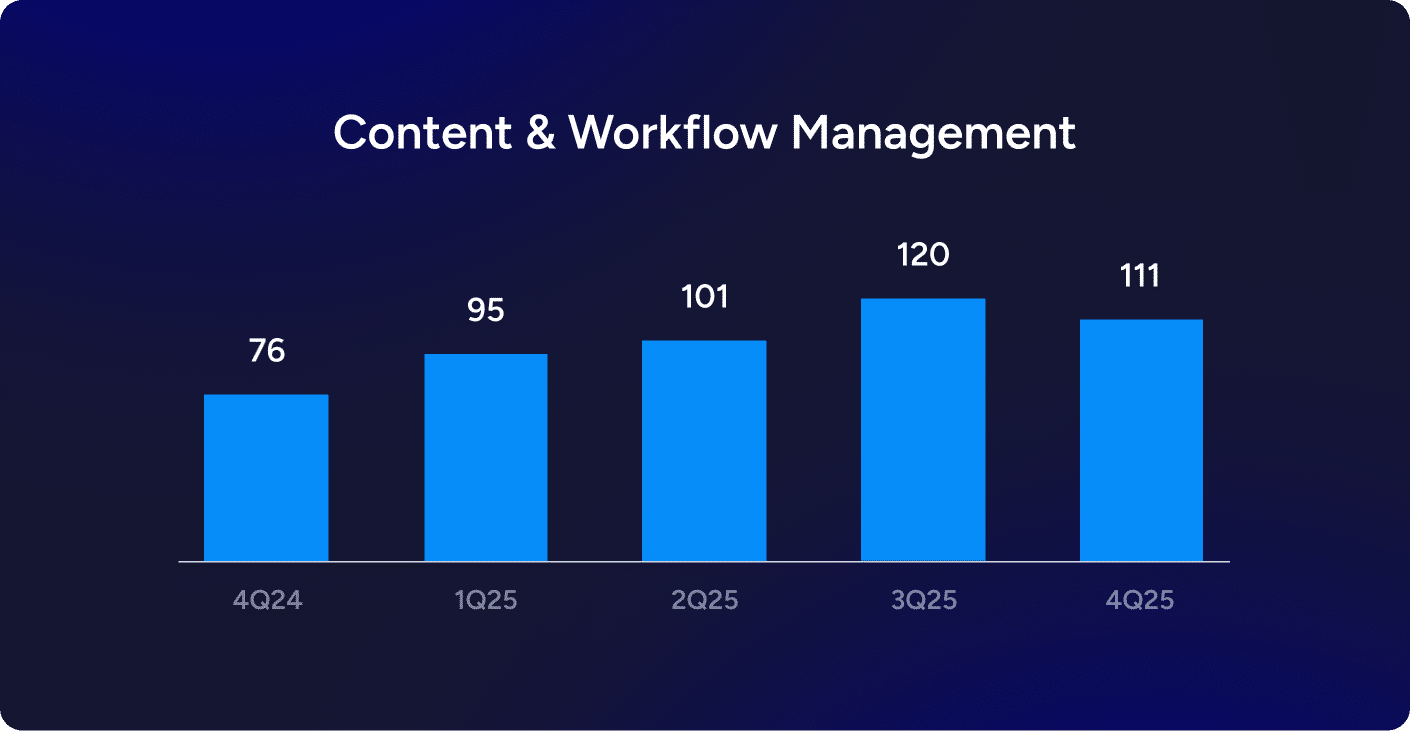

4. Content & Workflow Management

Core finding: AI is moving into the workflow layer, not just the analytics layer.

426 deals | Co-leading category | Healthcare dominates with 61 deals

Content & Workflow Management was one of the most active categories in 2025, matching Analytics & Data Management in total deal volume. But the activity here reflects a different kind of shift. This is the layer where work happens: where content and information is created, reviewed, approved, and acted on. In 2025, buyers focused on platforms that sit inside those workflows, particularly where AI can influence how tasks are completed.

Healthcare led all verticals in this category with 61 transactions, the highest of any vertical in any category. Deals like GE Healthcare’s $2.3 billion acquisition of Intelerad and Waystar’s $1.24 billion purchase of Iodine highlight demand for AI-powered systems embedded in clinical and administrative workflows.

In the horizontal segment, the same pattern holds. ServiceNow’s $2.85 billion acquisition of Moveworks and Automation Anywhere’s acquisition of Aisera point to a growing focus on AI-driven workflow automation, tools that both analyze and help complete work.

Even outside traditional enterprise workflows, the trend is consistent. Bending Spoons’ $1.308 billion acquisition of Vimeo reflects the increasing role of video as a core business communication and collaboration tool, rather than a standalone product.

Across the category, buyers were targeting platforms that sit at the point of action, where decisions are made and work moves forward.

What this tells us: AI is creating the most value when it is embedded directly into workflows, shaping how work gets done rather than sitting alongside it as a separate layer of analysis.

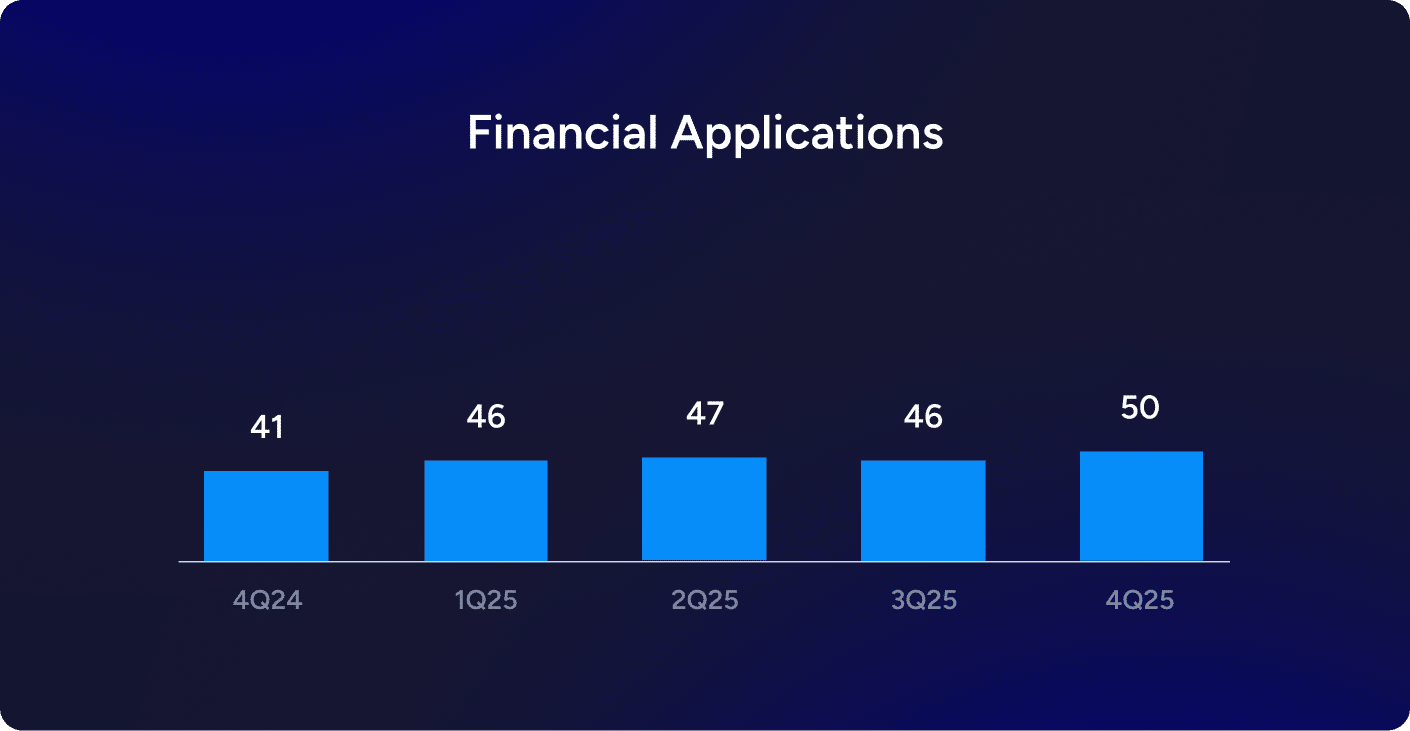

5. Financial Applications

Core finding: Payments infrastructure is consolidating, and digital assets are moving into the core.

189 deals | Largest single transaction across all categories (Worldpay) | Digital assets moved from fringe to embedded

Financial Applications produced some of the largest transactions in 2025, including the biggest deal across all categories: Global Payments’ acquisition of Worldpay at $24.25 billion. At the center of the category was payments infrastructure. Across the market, buyers targeted platforms that sit inside how money moves: accounts payable and receivable, payment orchestration, and treasury management.

Deals like TPG/Corpay’s acquisition of AvidXchange, Xero’s acquisition of Melio, and HG Capital’s majority investment in GTreasury reflect a consistent push to consolidate fragmented workflows into more unified systems.

Stripe’s activity reinforces that. Rather than focusing on a single niche, it made multiple acquisitions to expand across the broader payment stack, signaling a move toward end-to-end control of the enterprise payment workflow.

Along with that, a second shift became more visible. Digital asset infrastructure moved from the edge of the market toward the center. Established players including Ripple, Circle, and Galaxy Digital made acquisitions targeting custody, payments, and treasury capabilities tied to digital assets. Digital asset functionality is being integrated into existing financial systems, not treated as a separate category.

Taken together, the activity in this category points to consolidation at the infrastructure level, where control over how money moves, across both traditional and digital systems, is becoming more valuable.

In 4Q25, the median EV/TTM multiple was 5.3x in Financial Applications.

What this tells us: Buyers are prioritizing platforms at the core of financial workflows as the integration of digital assets changes the infrastructure layer of the category.

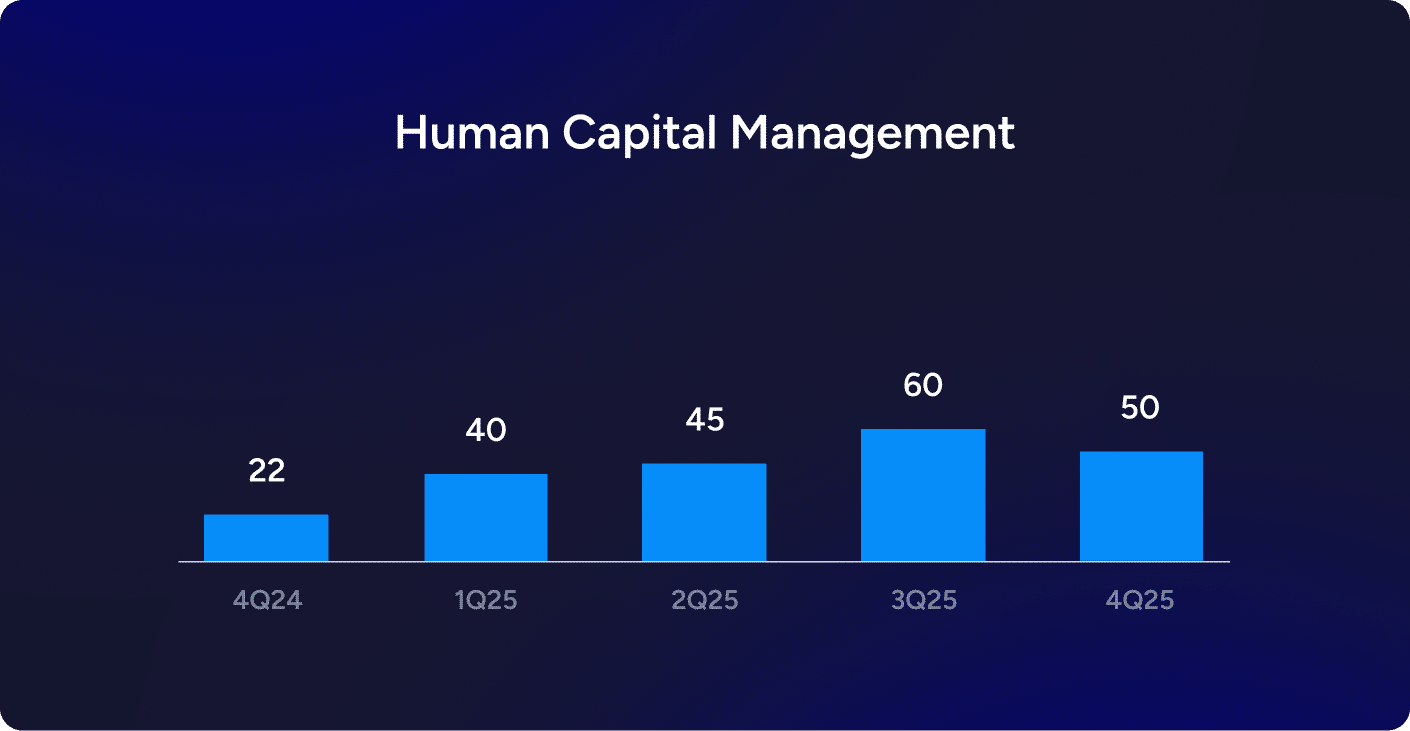

6. Human Capital Management

Core finding: Buyers are consolidating workforce platforms as employee data becomes more valuable.

195 deals | AI-native recruiting absorbed into platforms at pace

Human Capital Management was one of the most active categories in 2025, anchored by some of the largest transactions of the year, including the $12.3 billion take-private of Dayforce by Thoma Bravo.

But the headline deals point to a broader pattern. Buyers are consolidating large, embedded HCM platforms that sit at the center of how organizations manage their workforce, including payroll, benefits, compliance, and employee data. These systems are difficult to replace, which makes them attractive targets for buyers focused on long-term value and predictable cash flow.

The scale of take-private activity reinforces that. Transactions such as the Thoma Bravo-Dayforce deal, EQT’s acquisition of NEOGOV, Paymaster’s acquisition of Paycor, and others represent a significant concentration of capital in a single category. In each case, buyers are betting that these platforms are more valuable than public market valuations suggest as their underlying fundamentals improve.

At the same time, a second layer of activity has emerged. AI-native recruiting and talent acquisition tools were absorbed into larger platforms at a steady pace. Workday’s acquisition of AI company Paradox and multiple acquisitions by UKG and HumanlyHR indicate a push to integrate AI-driven capabilities directly into existing HCM systems, rather than leaving them as standalone tools.

Other segments, including learning and development and healthcare workforce management, followed a similar pattern, adding capabilities that extend the platform’s role across the full employee lifecycle.

In 4Q25, the median EV/TTM multiple was 4.7x in Human Capital Management.

What this tells us: Buyers are concentrating on scaled HCM platforms where workforce data is embedded and where integrating AI capabilities directly into those systems increases their long-term strategic value.

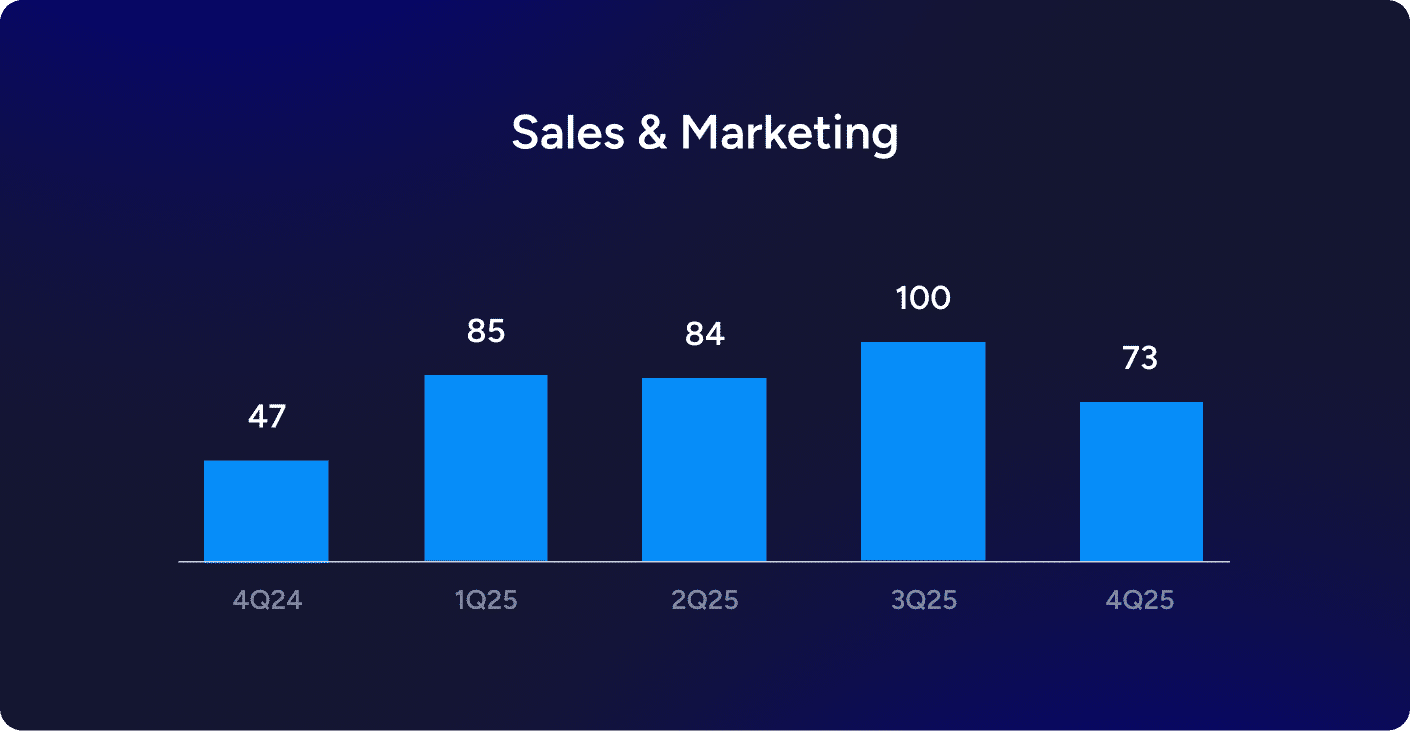

7. Sales & Marketing

Core finding: Strategic buyers are racing to transform the revenue workflow with AI.

342 deals | AI restructuring the revenue workflow at every level

Sales & Marketing saw heavy participation from established platforms, including Salesforce, Adobe, HubSpot, Intuit, and others acquiring capabilities at a steady pace. Qualtrics’ $6.75 billion acquisition of Press Ganey Forsta and Adobe’s $1.72B acquisition of Semrush both expand beyond point solutions into broader control of customer experience and demand generation workflows.

At the same time, AI-native sales and marketing tools were being absorbed into larger platforms. Deals such as the Clari/Salesloft merger, acquisition of Rightbound by Gong, purchase of Qualified by Salesforce, and HubSpot’s acquisition of Dashworks show that capabilities like automated prospecting, revenue orchestration, and AI-driven marketing are no longer standalone. They are being integrated into core systems.

Customer engagement platforms followed a similar path. Activity in loyalty, retention, and lifecycle marketing points to a shift away from point-in-time acquisition toward managing the full customer relationship. Even in advertising and media, buyers are repositioning infrastructure around where attention is moving, particularly toward connected TV and digital out-of-home channels.

Established platforms are moving quickly to expand their role across the entire revenue lifecycle before competitors do.

In 4Q25, the median EV/TTM multiple was 3.5x in Sales & Marketing.

What this tells us: This category is being driven by strategic urgency, as platforms race to integrate AI and consolidate control over the end-to-end revenue workflow.

8. Supply Chain Management

Core finding: Buyers moved early on scaled platforms, then shifted toward vertical solutions.

106 deals | Most front-loaded quarterly distribution | Three horizontal platform take-privates closed in Q1 | Trade policy context distinctive

Supply Chain Management saw more uneven activity than other categories, with deal volume heavily concentrated in the first quarter. That front-loading was driven by a small number of large transactions. Three horizontal platforms were taken private in Q1 alone, including e2open by WiseTech Global, Logility by Aptean, and 3GTMS by Descartes. Together, these deals removed several scaled, independent supply chain platforms from the market in a short period of time.

With fewer large horizontal platforms available, buyer activity then shifted toward more specialized, vertical solutions. Rather than acquiring broad, end-to-end systems, buyers focused on software built for specific industries and use cases.

Retail deals centered on inventory optimization and demand planning. Healthcare transactions targeted procurement and compliance workflows. Automotive and food supply chain platforms also saw activity, each tailored to the complexity of their respective industries.

The timing also reflects external factors. Much of the early-year activity occurred ahead of anticipated trade policy changes, which began to influence deal dynamics and valuation assumptions as the year progressed.

In 4Q25, the median EV/TTM multiple was 6.7x in ERP & Supply Chain Management.

What this tells us: Buyer attention is now focused on vertical supply chain software, where specialization and operational fit create differentiated value.

What Ties These Software Categories Together

In every category, the platforms that attracted the most sustained interest shared a common trait:

They sit inside critical workflows. Whether managing data, executing work, processing payments, or running industry-specific operations, these systems are embedded in how businesses function day to day.

That level of embeddedness creates durability. Replacing these systems requires reworking processes, retraining teams, and reconfiguring integrations. That translates into retention, which is one of the most valuable characteristics in software.

A second pattern across these categories is where AI is creating value.

Buyers showed a clear preference for platforms positioned in the path of AI adoption, including data infrastructure, workflow systems, and systems of record. AI is most impactful when it is integrated into how work is done, not layered on top of it.

Finally, vertical specificity continues to drive buyer behavior. In categories like Business Management, Supply Chain, and Asset & Facilities Management, the most attractive platforms were built for specific industries. These systems manage domain-specific workflows that are difficult for horizontal platforms to replicate, reinforcing their long-term value.

Taken together, buyers are concentrating on software that is embedded, operationally critical, and positioned to benefit from AI, not just in how it is marketed, but in how it is used.

What This Means for Software Founders and Operators

In every segment, buyers were selective. The companies that attracted the most interest combined strong positioning with clear evidence of retention, operational importance, and scalability.

Understanding where your product sits can be more important than how fast the broader market is growing. The companies that align with the patterns we covered in this article are more likely to attract sustained interest, regardless of overall deal volume.

Category-level data won’t tell you when to sell or what your company is worth. But it does provide something more useful: a view of how buyers are evaluating the market. And in a year as active as 2025, that context matters more than the headline number.

Additional Resources

- 2026 Annual SaaS Report: Full public and private market data for 2025

- SEG SaaS M&A Deal Database: Search and filter 2,698 transactions by category, vertical, and buyer type

- SEG SaaS Index: Track public SaaS performance by product category in real time

- SEG SaaS Scorecard: Benchmark your company against key buyer criteria

- The AI Reset: How SaaS Founders Can Reinvent, Defend, or Exit Stronger