An overview of our sell-side M&A services

SaaS Multiples 2025: What Does the Future Look Like for M&A Market Valuation?

SaaS valuations are stabilizing. Deal volume is rising. And interest in innovation-focused sectors is heating up. For SaaS companies with strong fundamentals, 2025 may be the best opportunity in years to attract premium valuations.

That’s the message from our 2025 State of SaaS M&A Buyers’ Perspectives Report and insights gathered during a recent private equity roundtable. Despite some early-year uncertainty, both buyer sentiment and CEO optimism point to a strong M&A landscape driven by durable growth, AI-readiness, and competition for high-quality targets.

Despite some economic headwinds and a somewhat slower-than-expected start to the year, the market for SaaS businesses in 2025 remains vibrant. That’s partly because unlike some other industries, the valuation of SaaS businesses is less subject to the volatility of larger macroeconomic forces and more a product of their own diligence, vision, and initiative.

Which means that SaaS businesses with a strong command of key metrics like the Rule of 40 and growth retention rates are well-positioned to take advantage of the current environment.

2025 SaaS Valuation Outlook: Stability for Most, Upside for the Best

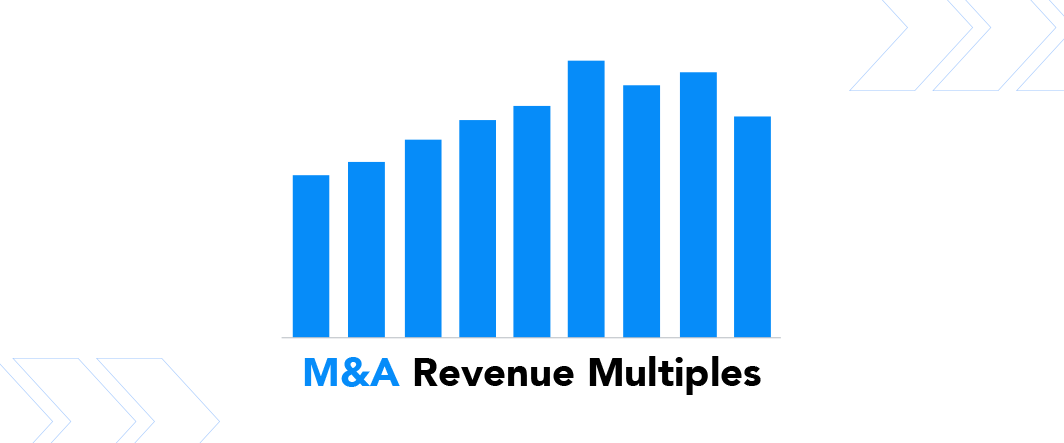

SaaS valuations have come down from the historic peaks of 2021, but multiples are holding steady and, in many cases, rising for top-performing companies.

According to SEG’s data, the median EV/TTM Revenue multiple for Q4 2024 was 4.1x, up 8% year-over-year. The average multiple hit 6.0x, the highest quarterly average since Q1 2023, driven by upside outcomes in the top tier of deals.

Three-quarters of SaaS CEOs expect valuations to stay stable or increase in the next year. This growth reflects a broader shift in sentiment:

- 57% of SaaS CEOs expect 2025 to be a better market than 2024.

- More than 40% of buyers anticipate rising valuations.

- 60% of CEOs say it’s a better time to seek investment or a liquidity event.

Deal activity is also picking up. SaaS M&A volume is now on par with pre-COVID levels, and experts expect that pace to hold or increase into 2025. Private equity firms report a noticeable rise in competition:

- 48% say the number of targets has increased.

- 53% are seeing more competition for those targets.

- 57% say the current environment is more competitive than in 2023.

CEOs are responding to this shift, with many expressing strong optimism about the year ahead. Fifty-seven percent of SaaS CEOs believe the market will improve in 2025, and nearly 60% expect 2025 to be a better time to seek external investment compared with 2024. This opens a window of opportunity for CEOs to explore liquidity events or strategic exits in a more competitive market Buyer preferences are evolving in response to emerging market trends. Buyers that once focused only on safe bets are now more open to companies in emerging verticals like AI and cybersecurity, especially when those companies pair growth with operational discipline.

What is Driving Higher SaaS Valuations in 2025?

The strongest valuation outcomes will go to businesses that can show durability, balanced growth, and strategic readiness. Durability and balanced growth are in vogue right now. Buyers are looking for sure doubles, not grand slams.

Here are the metrics and themes that matter most:

1. Revenue Retention

Retention remains a top differentiator. Companies with net revenue retention above 120% achieved a median 11.7x multiple in 2024 – more than double the industry median of 5.6x, according to our Annual SaaS Report. Yet surprisingly, 28% of CEOs still don’t track gross revenue retention, a blind spot in today’s market.

2. Sustainable Growth and Profitability

Growth alone isn’t enough. Unprofitable businesses are struggling to attract buyers, while those with efficient, high-margin models are commanding premium valuations. In Q4 2024:

- Companies with gross margins >80% had a median multiple of 7.6x.

- Companies below 80% gross margins earned a median of 5.5x.

3. AI Readiness

Buyers aren’t demanding fully built AI features, but they do want a clear-eyed view of the opportunity and the risk. CEOs who can articulate how AI will impact their operations, customers, or roadmap will stand out in a crowded market.

Most Attractive Verticals in 2025 for SaaS M&A

As buyer interest in purpose-built solutions continues to grow, vertical SaaS remains a hotbed of M&A activity. In 2024, 44% of all SaaS deals involved vertically focused companies, a strong signal of demand.

Buyers are drawn to vertical SaaS because these solutions are often mission-critical, deeply embedded in customer operations, and tailored to solve specific industry challenges. They tend to have higher switching costs, stronger retention, and clearer growth paths.

High-Demand Verticals

The most active sectors in 2025 include:

- Healthcare: Amid rising costs and mounting pressure on the U.S. healthcare system, providers and payers alike are accelerating digital transformation. SaaS solutions that support care delivery, compliance, and patient engagement are in high demand.

- Financial Services: With the cost of capital rising, banks, lenders, and fintech companies are turning to SaaS platforms to improve efficiency, automate workflows, and manage risk.

- Real Estate: Property management firms, brokerages, and asset owners are investing in cloud-based tools to modernize operations, improve tenant experiences, and enable data-driven decision-making.

Horizontal Categories Gaining Traction

While vertical SaaS continues to command attention, buyers are also active in horizontal software categories that address core business functions across industries. The most attractive horizontal categories right now include:

- Content & Workflow Management

- Business Management / ERP

- Sales & Marketing Enablement

- Security & Compliance

- Analytics & Data Management

Whether vertical or horizontal, buyers are prioritizing companies with a clear market focus, scalable architecture, and strong retention metrics.

What SaaS CEOs Need to Know: Positioning for Premium Valuations

For SaaS CEOs considering a liquidity event, strategic investment, or aiming to boost company value, the message from buyers is clear: Sustainable, metrics-driven growth is the path to a premium valuation. Here’s what matters most:

1. What Buyers Want

Retention is non-negotiable.

High gross and net revenue retention rates are key indicators of product-market fit and customer loyalty. Companies with net retention above 120% are earning valuations more than double the industry median.

Profitability signals discipline.

Growth is attractive when it’s efficient. Buyers are rewarding businesses with strong gross margins (>80%), steady cash flow, and a clear path to profitability.

A clear AI perspective stands out.

You don’t need to have AI fully integrated, but you do need a thoughtful plan. Buyers want to hear how you’re assessing the opportunities and risks of AI within your product, operations, and customer experience.

2. How to Prepare

Know your metrics cold.

Buyers expect CEOs to speak fluently about their Rule of 40 score, revenue retention, CAC payback, and other key benchmarks. If you’re not tracking a metric buyers care about, now’s the time to fix that.

Refine your story.

A compelling growth narrative, backed by data and anchored in a clear market need, sets you apart. This is especially true for companies in crowded or highly competitive sectors.

Build vertical credibility.

If you’re in a high-growth vertical like healthcare, real estate, or government, highlight your expertise and how your solution addresses critical challenges your customers face.

3. Strategic Timing Matters

Valuations are stable. Buyer competition is strong. And interest in innovation-driven and vertical SaaS is rising. If your fundamentals are in place, 2025 could be your moment to explore strategic options.

Position Yourself for Success: Take Charge of Your Story

Now is the time to get proactive. The M&A landscape in 2025 favors prepared, high-quality SaaS companies, and the right guidance can make all the difference. Our team of experienced M&A advisors can help you:

- Benchmark your business against market expectations

- Identify the metrics that matter most to buyers

- Craft a compelling story for your company

- Determine the right timing and strategy for a successful outcome

Don’t wait for buyers to come to you. Let’s position your business to lead the conversation.