An overview of our sell-side M&A services

ARR for SaaS Leaders: Its Impact on Valuation, Calculation, and Role in Growth Strategy

When a buyer evaluates your SaaS business, the first thing they zoom in on is Annual Recurring Revenue (ARR). Predictable ARR is what turns a software company into a compounding growth engine.

But even seasoned SaaS leaders often misunderstand how ARR should be defined, recorded, and communicated. Small mistakes can distort performance, mislead investors, and chip away at valuation.

In this article, we break down how to use ARR not just as a metric, but a strategic narrative that strategic buyers and private equity investors will pay a premium for.

What is ARR in SaaS?

ARR is the recurring revenue a SaaS business can expect to generate each year from subscriptions. Knowing how much revenue the company can count on from its core business (as opposed to one-off services or projects) makes it easier to make decisions and plan. That’s why ARR is one of the most important metrics to strategic buyers or private equity firms when determining valuations.

It answers the question they care about most:

“How much of this revenue will reliably show up again next year?”

When that answer is “almost all of it,” buyers lean in.

Strategic and private equity buyers both rank ARR in their top 3 when evaluating potential acquisitions. Learn more about what buyers are looking for in SEG’s Buyers’ Perspectives Report.

How to Calculate ARR for a SaaS Business

A SaaS company’s ARR should not include one-time charges such as set-up fees. Beyond calculating the value of current contracts, we also need to consider the dynamic nature of the business. Some customers may have upgraded their subscriptions to pay more (expansion revenue), while others may have downgraded their subscriptions or canceled their contracts (called Customer Churn).

Given this, here is the ARR formula:

Prior-Period Annual Subscription Revenue + New Subscription Revenue + Expansion Subscription Revenue – Churned Subscription Revenue = Current ARR

For example, say your company’s total revenue from subscriptions last year was $4.5M. This year, you sold $1.5M of new subscriptions. You also sold $200,000 of upgrades (expansions). Throughout the year, customers leaving or downgrading amounted to a $1.5 million decrease. The resulting calculation would look like this:

| Last Year’s Subscriptions | $4,500,000 |

| + Net New Subscription Agreements | $1,500,000 |

| + Upgrades (Expansion) | $200,000 |

| – Downgrades (Churn) | $1,500,000 |

| = ARR | $4,700,000 |

What ARR Tells Buyers in SaaS

Not all ARR is created equal, and buyers price accordingly. Buyers look at how durable it is, how efficiently it grows, and how much confidence they can place in its expansion. Two companies can have $10 million in ARR and receive different valuation outcomes depending on retention rates, customer concentration, and the capital required to fuel new growth and maintain the current base. ARR efficiency and predictability matter.

Here’s what buyers are looking at:

Revenue Stability

ARR gives buyers insights into the stability of a SaaS company’s revenues. High Gross Revenue Retention (GRR) indicates your ARR is durable because customers stay and see value. Strong Net Revenue Retention (NRR) demonstrates your ARR can grow efficiently through expansion, not just acquisition.

Historical Performance

Buyers don’t evaluate ARR in isolation; they look at how it has behaved over time. Past growth rates, margin trends, and retention performance are among the strongest indicators of future outcomes. Consistent growth and improving margins signal an ARR base that can scale efficiently and predictably.

Customer Base

The composition of ARR speaks to the quality of a customer base. This includes customer counts and types, contract terms, renewal rates, and cohort growth rates. Longer contract terms and favorable renewal structures improve predictability, while a customer mix skewed toward larger, repeat buyers typically results in stronger retention and expansion rates. Customer concentration is also a consideration for most buyers. Low customer concentration makes ARR more stable because no single customer can materially impact revenue.

Synergy Planning

Understanding a target company’s ARR helps a buyer plan for integration. It informs decisions around customer onboarding, retention strategies, and cross-selling opportunities. These are all vital for post-acquisition growth.

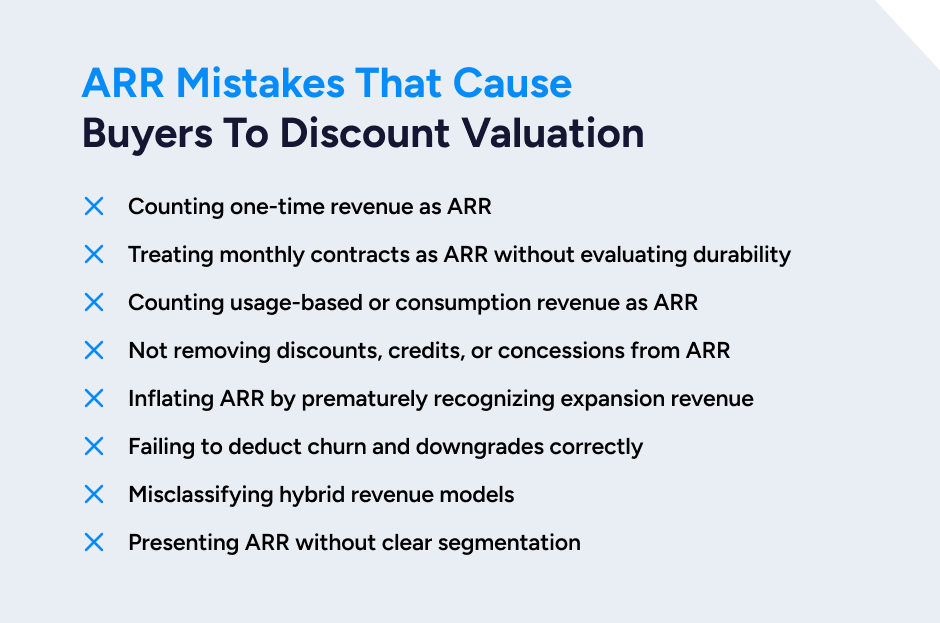

ARR Mistakes That Cause Buyers to Discount Valuation

Buyers don’t just accept your ARR number at face value; they rebuild it from the ground up. They separate recurring from non-recurring, strip out anything that looks opportunistic, and test whether your definitions are consistent over time.

Here are some of the most common mistakes buyers see when founders calculate and present ARR, and how they’ll adjust for them.

Counting one-time revenue as ARR: Examples include implementation fees, training and onboarding revenue, services or customization projects, and one-off contract add-ons. This matters because adding one-time revenue to the calculation incorrectly inflates ARR.

Treating monthly contracts as ARR without evaluating durability: Buyers commonly annualize monthly recurring revenue by multiplying current MRR by 12. But they do not treat all monthly revenue as equally durable. When revenue has no minimum term commitment or elevated churn, buyers may discount it because predictability is lower. The issue is not the billing cadence, but whether historical retention supports treating that revenue as truly recurring.

Counting usage-based or consumption revenue as ARR: Usage-based revenue can be highly recurring in practice, but it is not contractually committed. Buyers typically separate committed recurring revenue from variable or consumption-driven revenue and analyze it more heavily to understand volatility, customer behavior, and downside risk.

Not removing discounts, credits, or concessions from ARR: Some teams calculate ARR based on list price rather than actual billed amounts. This is a red flag for forecasting, and will usually lead to a restatement downward of ARR.

Inflating ARR by prematurely recognizing expansion revenue: This may include counting pipeline expansions as ARR; counting a signed upsell before it’s activated; or counting contracted expansions before implementation or revenue recognition.

Failing to deduct churn and downgrades correctly: A common issue is using new recurring revenue but ignoring contraction; not updating ARR on a cohort basis; applying churn only annually instead of monthly or quarterly. This artificially smooths volatility and misrepresents retention.

Misclassifying hybrid revenue models: Companies may misclassify revenue streams as ARR when they’re really pay as you go, transactional, marketplace margins, or service components bundled in a subscription. Buyers will separate these.

Presenting ARR without clear segmentation: Buyers want to know how ARR breaks down. For example, new vs. expansion vs. renewal by product line; by customer size/vertical. This type of data helps buyers judge scalability and risk.

How to Improve ARR Quality Ahead of a Sale

Potential buyers want to identify anything that could undermine future revenue visibility. ARR patterns that may trigger concern include:

- High churn hidden beneath new logo growth (signals the company may not have found product-market fit)

- Heavy reliance on professional services (which doesn’t scale)

- Over-discounting to win business (indicates competitive pressure or weak product differentiation)

- Too much revenue tied to one customer or segment

These can compress valuations because of the quality of ARR and the risk attached to it. Addressing issues like these early protects your negotiating leverage long before a sale is underway.

Improving revenue quality is about reducing risk while increasing durability and expansion potential:

- Strengthen onboarding and early adoption to improve retention and reduce reliance on new-logo growth

- Refine pricing and packaging to better align value delivered with value captured, increasing expansion ARR

- Convert one-off services into recurring offerings to add predictability and improve gross margins

- Reduce concentration in a small number of accounts to lower perceived customer-level risk

Buyers want revenue that can grow without adding headcount at the same time. They want to understand not just how much revenue exists, but how it behaves over time. Post-acquisition value creation depends heavily on repeatability.

ARR vs. Similar SaaS Revenue Metrics

Here’s how ARR compares with related metrics.

ARR vs. MRR

An alternative way to calculate ARR is to simply multiply your MRR (monthly recurring revenue) by 12. Annualizing a single month’s recurring revenue gives you a point-in-time view of your run-rate ARR. Similarly, you can divide your ARR by 12 to arrive at your MRR.

ARR vs. Revenue

Revenue can refer to any source of income the company receives (whether recurring or not) from its operations. The term “revenue” by itself should not be used as a substitute for annual recurring revenue.

ARR vs. Reoccurring Revenue

The terms “recurring” and “reoccurring” are often used interchangeably, but this can be misleading when referring to revenue. While recurring refers to revenue that is predictable at specified intervals (like any type of subscription), reoccurring should be used to describe purchases a customer makes repeatedly, but with no pre-designated or contracted regularity. This type of revenue may or may not be included in an ARR calculation.

ARR vs. Transactional Revenue

Unlike contractually recurring revenue, transactional revenue comes from charging customers on a usage basis rather than through subscriptions. An example of transactional revenue would be when an ecommerce payment platform receives a small fee for every purchase made through its system. Like reoccurring revenue, the nature of the revenue and predictability will determine if it is included in the ARR calculation.

ARR vs. One-Time Revenue

When a customer purchases a product or service with no expectation of repeat purchases, it’s called one-time revenue. SaaS companies may receive some one-time revenue for set-up/training fees or support. These would not count toward ARR.

ARR vs. Contracted (or committed) Annual Recurring Revenue (CARR)

This metric provides another view of recurring revenue that also includes bookings (new customers who have yet to start paying). CARR gives a more forward-looking view than ARR, which is helpful if customers don’t typically go live until months after they sign a contract or if the company is growing quickly. This information will also be important for prospective buyers when evaluating your company.

ARR vs. Bookings

A customer is considered booked when they sign a contract, even if their go-live date has yet to occur. Bookings are not included in the ARR calculation but would be included in CARR.

ARR vs. Billings

Not to be confused with bookings, billings refer to customers who have gone live and are actively paying for the use of the software. Billings for subscriptions are included in the ARR calculation.

How to Turn Your ARR Into a Premium Outcome

High-quality ARR gives buyers confidence: confidence in predictable cash flows, confidence in durable retention, and confidence that future growth will compound rather than reset.

When you understand the drivers behind your ARR, you gain control. Control over how you run the business today, and control over how you position it when you eventually go to market. Buyers pay premiums for clarity, discipline, and predictability. A clean, defensible ARR story delivers all three.

As you plan your long-term strategy or prepare for an eventual exit, having a seasoned SaaS M&A advisor in your corner becomes essential. Software Equity Group has spent more than 30 years helping founders turn their ARR into a strategic narrative that strategic and private equity buyers compete for. If you’re ready to understand how buyers will view your business, and how to maximize that outcome, let’s talk.