An overview of our sell-side M&A services

How to Select the Right Buyer for Your SaaS Company’s Next Chapter

Many founders assume buyers hold more power in an acquisition. But that mindset can hurt you when it’s time to sell.

Not only do SaaS leaders have the ability to choose who they sell to, it is one of the most important decisions they make. Don’t give up that power by taking the first offer that comes along.

Having spent the last 15 years of my career working on both the buy side and the sell side of SaaS M&A, I’ve seen firsthand how founders and buyers evaluate one another and how alignment, or the lack of it, can shape what happens after the deal closes. The most successful outcomes rarely come down to price alone. They come from fit between people, priorities, and long-term vision.

Your choice will shape your future after the sale. It influences everything from team retention and customer experience to your own role post-close. It’s a decision worth extra scrutiny.

Valuation Matters – But It’s Not the Whole Story

Don’t focus solely on the valuation when you consider what it means to you to have a successful exit. Founders usually have a mix of financial, strategic, and personal goals. Some want to secure a full sale and then step back into retirement. Others want to stay involved with a partner to accelerate growth. Most care deeply about cultural fit and long-term direction, not just the dollar amount.

The right buyer depends on your priorities. Look at each buyer through the lens of culture, growth goals, and financial outcomes so you can choose a true partner and not just the highest bidder.

Mark and Lori Smith, founders of Core Sound Imaging, say that the buyer SEG ultimately helped them find won because they brought more to the table than just a number.

“It wasn’t the valuation alone for sure. I would say that was the smallest piece of it. The offer had other components, things that we just really felt we needed.”

Early on, the Smiths had found a couple of possible offers on their own, and “the easiest thing for [SEG] would’ve been to encourage us to take one of the offers.” But SEG invested the time to make sure it was a true fit: “They really heard us, and they didn’t think it was the right path if we weren’t interested in doing that.”

The process of finding the right buyer often starts long before you go to market. The best outcomes often come from relationships built early. Founders should pick five to 10 firms that really know their space and invest time getting to know them. Those early conversations give both sides confidence and reveal which buyers share your values, understand your industry, and follow through on their word. By the time you launch a process, you already have some interested parties lined up who won’t take long to get up to speed; these parties can really help drive a competitive process.

How to Match Buyers’ Playbooks to Your Priorities

Buyers also come to the table with their own mix of goals and expectations.

Some buyers bring operational expertise and growth capital but expect rapid scaling and their own future exits. Others prioritize strategic integration, long-term stability, or cultural fit. Understanding these differences early helps founders understand a variety of different lenses with which an investor will view their company and can help them gain a better understanding of alignment with their vision for the company, team, and their own role after the deal.

Different buyers (strategic acquirers, private equity firms, PE-backed platforms, minority investors, and search funds) bring different lenses to how they view to ownership, growth, and integration.

Selecting the right buyer requires more than comparing price tags. It means evaluating alignment across growth plans, deal structures, leadership roles, and post-close priorities so the outcome matches your vision for the company and its team.

John Halloran, cofounder of Mobile Health, reflects that a motivating factor in selling his company that competitors were consolidating. That led Halloran and his cofounders to seek a larger platform and partner. They felt that by doing so, their solution could help more customers. Trying to expand their reach independently was holding them back.

The SaaS Buyer Landscape

Here’s a quick field guide to the types of buyers you might encounter in a competitive M&A process. Every buyer is different, but these common profiles can help you understand their typical goals and approaches.

- Public strategic buyers typically focus on expanding product lines, entering new markets, or acquiring specialized tech and talent.

- Private strategic acquirers make targeted acquisitions that emphasize product fit, customer overlap, or new markets.

- Private equity platforms are profitable, scalable SaaS companies that can serve as a foundation for add-ons.

- PE-backed strategic buyers seek growth through add-ons that expand capabilities, share, or efficiency.

- Minority investors and growth equity provide capital for partial ownership, but they can create governance or exit challenges.

- Search funds raise capital from investors to identify and acquire a privately held company, ideally one that’s profitable and owner-operated. After the sale, the searcher steps in and operates the business for several years, with the ultimate the goal of selling it to create ROI for investors.

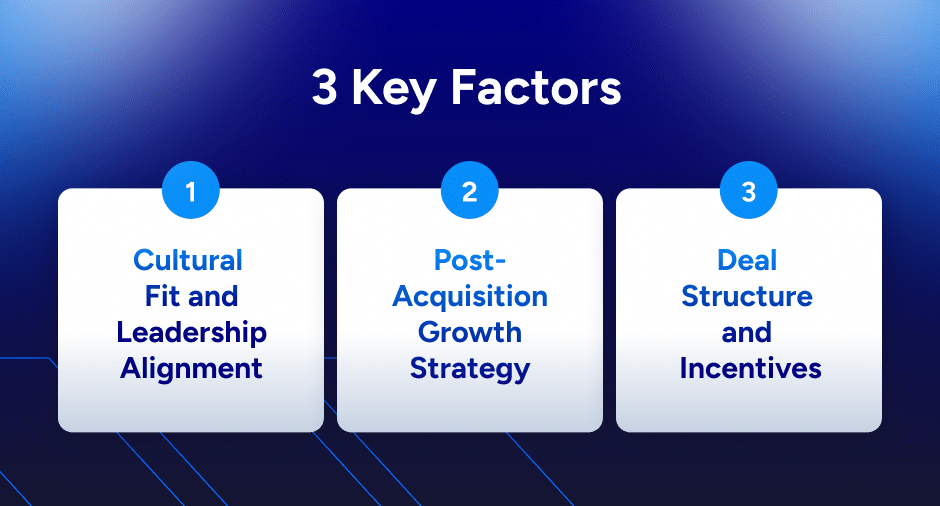

To navigate these options, focus on three key factors:

Factor 1. Cultural Fit and Leadership Alignment

Too often, founders underestimate the long-term impact of cultural alignment and leadership philosophy. Yet these factors affect everything from team retention and morale to product strategy and day-to-day decision-making after the deal closes.

- Strategic acquirers, for example, might fully integrate your company into a larger organization, which will bring access to more resources but also a shift in decision-making.

- On the other hand, private equity firms might leave leadership largely in place while layering in operational best practices.

- And at the opposite end of the spectrum, a search fund may replace leadership altogether, taking the reins themselves.

None of these choices are inherently better or worse. The right choice depends on your priorities as a founder. During discussions, ask specific questions about how the buyer sees your leadership team’s role after the deal, including what decision-making authority you’ll retain and how they’ve managed past integrations.

Buyers are also looking for the right fit. The right buyer shares conviction in your mission and vision.

Don’t hesitate to reach out to other founders who have sold to the same buyer. Their experiences can offer valuable insight into what life during the deal dilligence and negotiation and what it is really like after closing.

Factor 2. Post-Acquisition Growth Strategy

One of the biggest differences among buyer types is how they approach growth.

Strategic buyers may want to combine your company with existing products or business units to increase cross-selling and create integrated solutions. For founders seeking faster market penetration or access to a larger customer base, this can be a natural fit.

Some private equity buyers, on the other hand, focus on building value for a future exit. They may use a buy-and-build strategy, acquiring complementary businesses to form a larger platform. For founders interested in a second bite at the apple, this model can be attractive, as it often allows for rolling equity.

Understanding each buyer’s growth strategy and long-term vision helps you anticipate how your company will evolve under new ownership and whether that aligns with your own goals.

Factor 3. Deal Structure and Incentives

Not all offers are created equal, even when the valuations look the same. In fact, two similar headline prices can have very different outcomes.

That’s because deal structure can significantly affect both the risk and the potential upside for founders. For example:

- Earnouts tie a portion of the purchase price to future performance milestones. They can be appealing if you’re confident in the company’s growth potential under new ownership.

- Equity rollovers let you retain partial ownership and participate in the company’s next phase of growth.

- All-cash deals provide immediate liquidity but no future upside.

Private equity buyers often favor rollovers and incentive structures that align interests for a future exit and enable them to stretch on a valuation while not having to deploy the cash all at once, while strategic buyers may prefer all-cash deals.

To navigate these options, weigh not just the size of the offer but the balance of risk, control, and future upside each structure creates. Pay attention to RWI (Representations and Warranties Insurance) and holdbacks, as well. What indemnities apply, and how much protection do they provide?

Consider this example:

- Offer A: $200M valuation with a $35M earnout, restrictive terms, and no RWI support. You walk away with $158M and lots of potential risk.

- Offer B: $200M valuation with a low escrow, clean reps, and a founder-friendly structure. You net $198M.

Both deals carry the same headline price, but they delivery vastly different outcomes.

Understanding how to negotiate structure what turns a $200M offer into a $200M payout. Expert advisors can help you sort through the complexities and zero in on the differences that matter.

How to Test for Long-Term Compatibility

Even when early impressions are positive, there‘s a higher bar when it comes to long-term compatibility. Ideally, you want a buyer you wouldn’t mind being trapped in an elevator with because you’re going to be working closely together for the foreseeable future, facing whatever challenges the months and years ahead may bring.

With the right chemistry, the payoff can go far beyond the deal price itself. I’ve seen buyers help founders rediscover the spark for the business, reigniting their passion for the next chapter while giving them more time with their families. That’s a classic win-win.

As you move deeper into the process, focus your conversations on assessing future compatibility. Ask questions like:

- How do you measure success for your portfolio companies or acquisitions?

- What resources will you bring to accelerate growth after the acquisition?

- How involved do you expect founders and leadership teams to be after closing?

- What is your typical hold period, and how do you approach future exits or liquidity events?

These are not the only questions to ask, but they’re a good start. The answers will help you compare buyers on more than valuation, so you can choose a partner who’s most aligned with your vision for the company, the team, and your own future role.

Jessie Yu, former CEO of EcoInteractive, captured this idea perfectly when reflecting on finding the right buyer for her business:

“We felt like the best home for Eco was still somewhere that had so much conviction, just as much as our board and myself did, in investing in the organic and inorganic opportunities that we could take advantage of.”

She also emphasized the value of expert guidance during the process:

“When you have different types of buyers, how do you assess real intent and how do you decide when to keep someone in a process or not? There were moments in the process where there were counterintuitive decisions that we made at SEG’s behest that completely transformed, I think, the final outcome in a positive way.”

Fit Over Finish Line: Making the Right Long-Term Choice

Trust matters at the decision stage. Ask yourself: Is this a company I’d invest my own money with? Would I roll my equity with them? The answer will tell you everything about fit.

Choosing a buyer is a little like deciding who will care for your business after you. As a founder, you’ve poured your heart and years of your life into building it. Now it’s time to consider who will best protect your team, culture, and vision so they can continue to grow and thrive.

While valuation is important, it’s only one part of a much larger decision. If Buyer A is offering $40 million and Buyer B $39 million, what will you do with 40 that you couldn’t do with 39 if you trust Buyer B more? The right buyer will be best aligned with your company’s next chapter.

With an experienced advisor in your corner, it’s often possible to achieve both: a strong valuation and the right long-term fit. Founders who approach this decision thoughtfully avoid post-acquisition regret and often see smoother integrations, stronger growth, and better outcomes over time.

Whether you’re weighing early inbound interest or preparing for a formal process, start by clarifying your goals, evaluating buyers against structured criteria, and partnering with advisors who can help you run a process that protects both valuation and vision.

Ready to explore your options? Get in touch to start a conversation with our team.