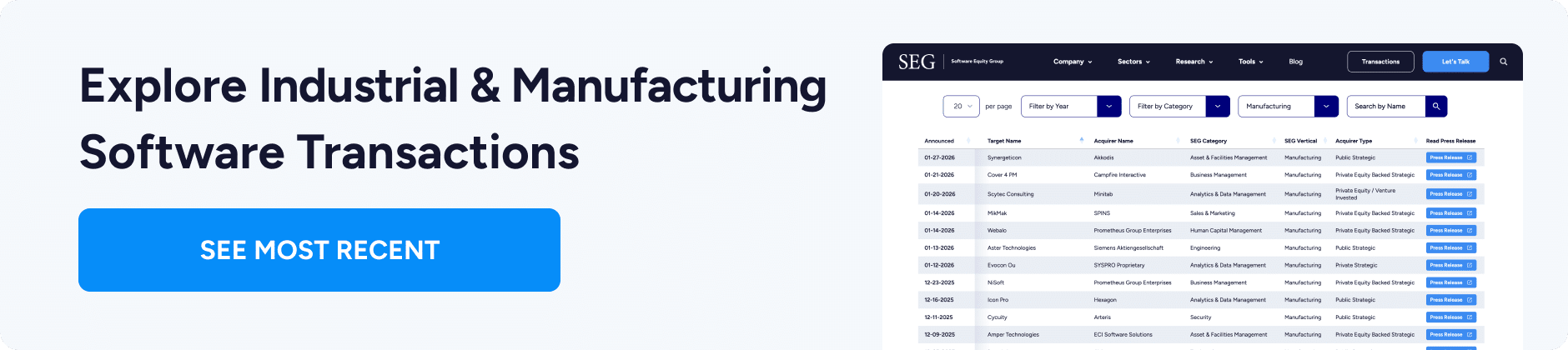

An overview of our sell-side M&A services

Industrial and manufacturing software is entering a structural shift.

Sustained volatility, workforce compression, and supply chain fragility are redefining how manufacturers evaluate technology and how buyers evaluate software companies serving the sector. This report examines where demand is durable, where value is concentrated, how AI and connected architectures are reshaping competitive dynamics, and what drives premium outcomes in today’s M&A market.

Strategic Questions This Report Answers:

- Is industrial and manufacturing software structurally expanding?

We analyze macro forces, policy tailwinds, and operational volatility to assess whether software demand is cyclical or structurally durable. - What are manufacturers prioritizing right now?

From uptime and workforce reinforcement to real-time visibility and coordinated execution, we examine how buying behavior is shifting under sustained pressure. - How should you approach architecture and AI?

We explore the transition from hierarchical systems to connected data ecosystems, and what Industrial DataOps, Unified Namespace models, and AI orchestration mean for product strategy. - Where do you sit in the industrial and manufacturing software landscape?

We define the functional domains underpinning modern manufacturing and clarify how systems of record, operational platforms, and intelligence layers interact. - What are buyers rewarding in this market?

We break down deal velocity, buyer mix, and category momentum to identify where strategic and PE-backed acquirers are concentrating capital. - What drives premium valuations in industrial and manufacturing SaaS?

Using SEG’s 22 Factors framework, we connect retention, architecture, workflow depth, and growth efficiency to long-term enterprise value.