An overview of our sell-side M&A services

SaaS M&A Snapshot: Target Market & Buyers

The public markets may have taken a beating, but behind the gloom-and-doom headlines, there was still plenty of good news for private SaaS companies in 2022.

On the surface, things looked rough: the Dow Jones, S&P 500, and the NASDAQ all finished the year with significant losses, with tech stocks hit particularly hard. The SEG Index, a collection of 116 public SaaS companies, fell by 48.2%. After the unprecedented market highs of 2020 into 2021, it’s natural for founders in this environment to wonder if they’ve missed the boat.

But although the environment has certainly changed, private markets have a different story to tell. While median EV/Revenue multiples declined from 4Q20–1Q22, they still outperformed the median public market multiple, and SaaS M&A deal volume jumped to a new record. Despite the macroeconomic uncertainty, buyers and investors are still willing to pay a premium for mission-critical, recession-resistant companies.

Following are some highlights of SaaS M&A deal activity over 2022. For a more in-depth look at our research, download SEG’s Annual 2023 SaaS Report.

SaaS M&A Metrics from 2022

SaaS Deal Volume

Although the number of SaaS M&A deals declined with each quarter, the overall annual volume was exceptionally healthy, jumping to a record of 2,157, a 21% increase over 2021. Despite the QoQ decline, the year still finished strong with 469 deals in 4Q22. While some public strategics backed off, they were more than made up for by private equity companies with plenty of dry powder and a healthy competitive environment.

Although the number of SaaS M&A deals declined with each quarter, the overall annual volume was exceptionally healthy, jumping to a record of 2,157, a 21% increase over 2021. Despite the QoQ decline, the year still finished strong with 469 deals in 4Q22. While some public strategics backed off, they were more than made up for by private equity companies with plenty of dry powder and a healthy competitive environment.

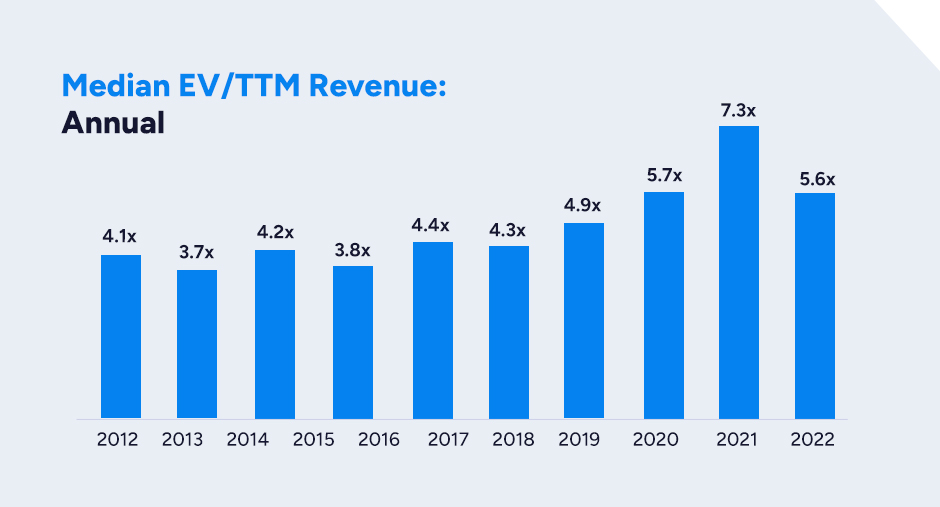

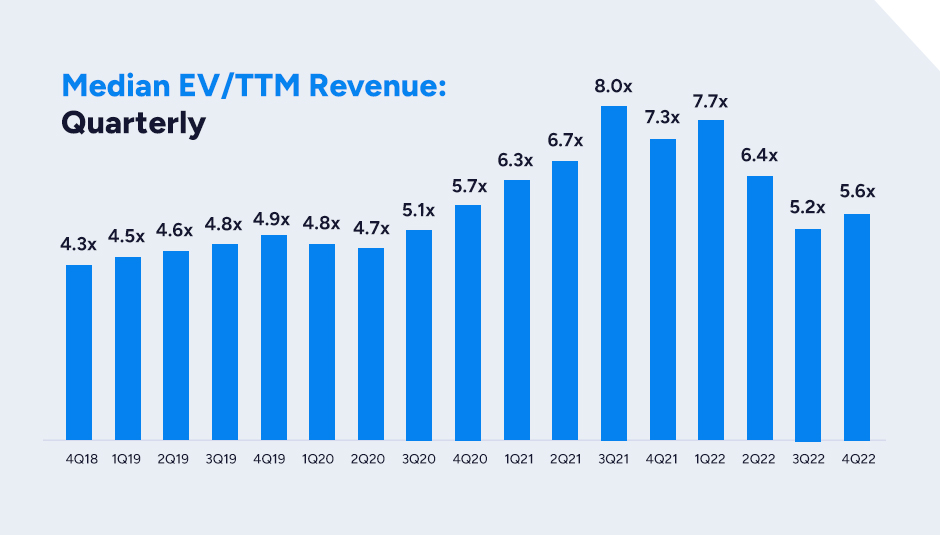

Median EV/TTM Revenue Multiple

Down from 2021’s high of 7.3x, 2022’s median EV/Revenue multiple of 5.6x was only a slight decline from 2020’s 5.7x and comfortably higher than pre-pandemic levels. After the market exuberance of 2020 and 2021, peaking at 8.0x in 3Q21, we are now looking at a return to more normal levels. 4Q22’s multiple of 5.6x speaks to a healthy environment, with multiples shored up by private equity buyers on the hunt for high-quality assets.

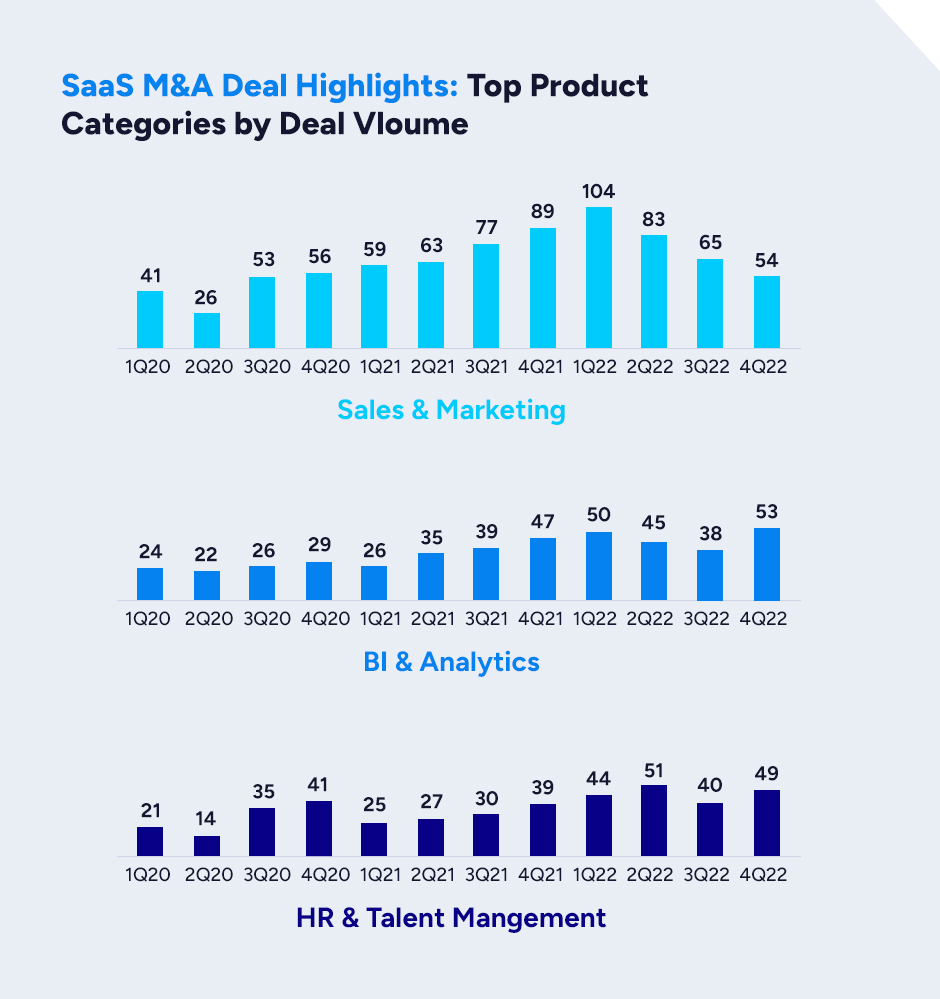

Top Product Categories by Deal Volume

With 306 deals, Sales and Marketing was the most active category in 2022—and in 2021 and 2020 as well. BI & Analytics hit a personal best with 53 deals in 4Q22 and had 186 deals altogether. HR and Talent Management came in a close third place with 184 deals for the year. Interest in these categories was reflected in rising public market revenue for BI & Analytics and HR & Talent Management, speaking to the demand for business intelligence and the tight labor market of 2022.

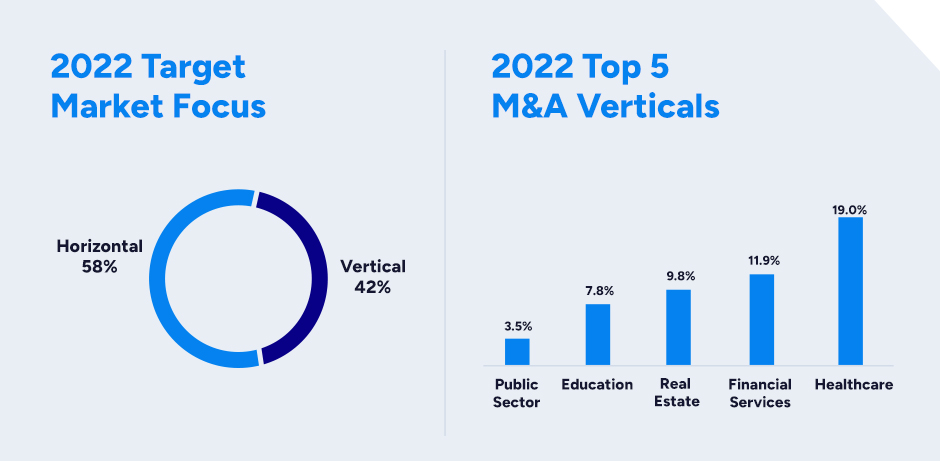

Target Market Focus

We usually see a 60/40 split in transactions involving horizontal vs. vertical markets. In 2022, verticals made up 42%, a slight increase. In terms of the target market, the top five SaaS verticals were led by Healthcare, as more and more companies in the healthcare sector turn to SaaS solutions to improve patient care and manage costs.

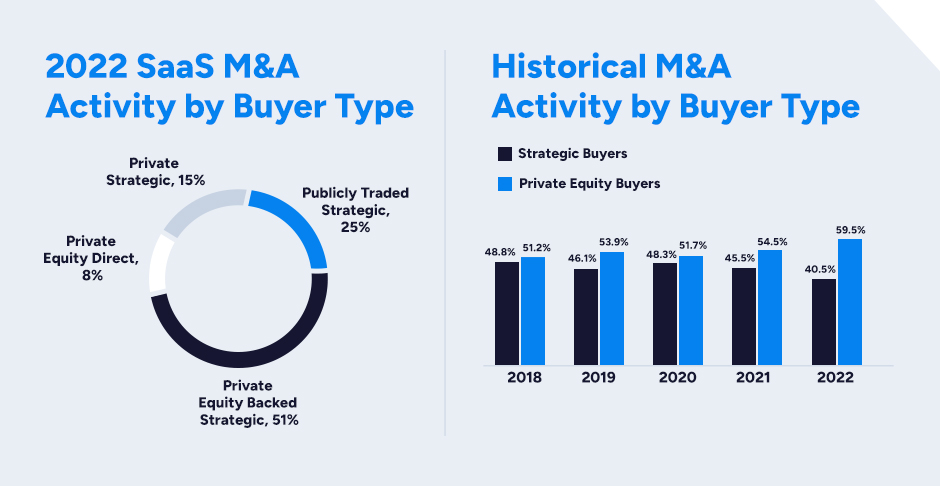

Buyer Backing

There are two primary groups of buyers in the world of SaaS: financial and strategic buyers. Financial buyers are either private equity (PE) firms with a fund or thesis targeting a type of software, or they can be PE-backed strategic companies with financial backing from a PE sponsor. Strategic buyers are publicly traded or privately owned software companies.

Private equity direct and private equity-backed strategic buyers together made up 59.5% of all SaaS transactions, a significant increase from previous years. On the other hand, public and private strategic buyers fell from 45.5% in 2021 to 40.5% in 2022. Particularly notable is the significant decline in public strategic deals, which fell from 35% to 25% from 2021 to 2022.

What Does This Mean for Founders and Private Companies?

In previous economic downturns, such as 2008, private SaaS company valuations took a hit as public strategics were forced to cut back. In those earlier downturns, however, private equity was not yet investing heavily in SaaS, but that has changed over the past several years. Today, the majority of M&A transactions are by private equity companies or private equity-backed strategics.

“There’s a comfort and safety net that did not exist in previous down cycles,” says SEG Vice President Austin Hammer. “Founders see public equity going down and assume everything is bad, but we have a highly acquisitive private equity environment with capital to be deployed. The capital is still there; you just need a quality company.”

And quality, according to Austin, lies in retention, profitability, and growth. Buyers and investors are looking for companies in durable, recession-resistant markets with strong prospects for growth and profitability and high retention rates. Private SaaS companies that meet these criteria continue to find buyers and investors, and M&A valuations for these businesses will likely continue to outperform the median.

You can find more details in our Annual SaaS Report 2023. We have researched the state of the public SaaS market as well as M&A deal activity across the software industry to create a comprehensive analysis of the SaaS market as a whole, including historical deal volume by product category and vertical, valuation statistics, most active buyers, notable deals, private equity activity, and more.