Our Services

An overview of our sell-side M&A services

Understanding how net ARR retention contributes to valuation is important for SaaS founders looking forward to an investment or exit. After all, when given the proper focus and resources, retention becomes the gift that keeps on giving (in valuation dollars, at least).

To help SaaS businesses understand the importance of net retention, SEG Managing Partner Allen Cinzori teamed up with SaaS Capital and ChurnZero in a joint webinar to present an entirely new perspective on the interrelationship between valuation, ARR growth, and net retention — all in one chart.

In this blog, we break down the key takeaways of SEG’s net ARR retention wave from the webinar to help founders understand how net ARR retention affects valuation.

Various factors contribute to a company’s valuation, including both qualitative and quantitative measures. However, few metrics have a more demonstrable impact on SaaS company valuation multiples than net dollar retention (more on this later).

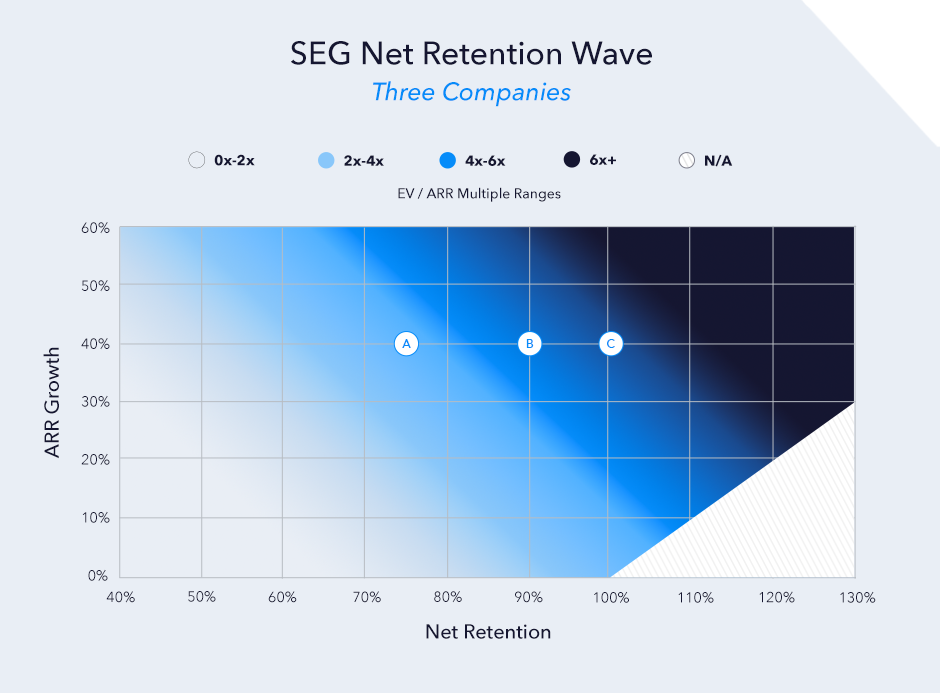

That’s why, in order to better understand how the correlation between ARR growth and net retention impacts a SaaS company’s valuation, we decided to analyze and plot data for SEG SaaS Client multiples (primarily in the lower to middle markets) over the past few years. We discovered wave-like patterns correlating with valuation for every improved net retention score. Check out the chart below.

Click to View PDF of Net Retention Wave

Chart Note: Larger SaaS businesses should expect multiple expansion. This chart mostly represents SaaS sellers in the lower to middle markets.

In order to better understand the net ARR retention wave, let’s start things off simple with an example. Picture two boats on a lake. Let’s call them Rowboat A and Rowboat B. Three people are in each boat, and the boats are floating at the same waterline. If the waterline is a metaphor for ARR growth, both boats appear to be “growing” at the same rate.

However, if we look a bit closer, it turns out the boats are in very different situations. Inside Rowboat A, the three people are working feverishly to bail water from the boat. Meanwhile, the three people in Rowboat B are comfortably sitting under an umbrella drinking Mai Tais.

If the activity going on in the boat represents the internal sales and retention flow of the business, Rowboat A clearly has to do more work than Rowboat B when it comes to staying at the same waterline (ARR). So, which boat do you want to be in long-term? Which boat is more valuable? Clearly, Rowboat B.

Taking this back to the real world, let’s answer this fundamental question: Why does net ARR retention play such a large role in determining valuation? We’re glad you asked.

Net ARR retention looks at retention on a dollar basis. It’s defined as the sum of customer expansion ARR, contraction ARR, and lost ARR, divided by the company’s beginning of year ARR (learn more about calculating churn here).

Consider three companies with 40% ARR growth. Company A has 75% net retention and is in the 2x – 4X ARR range. Company B has 90% net retention and is in the 4x – 6x ARR range. Lastly, Company C has 100% net retention and is in the 6x+ ARR range.

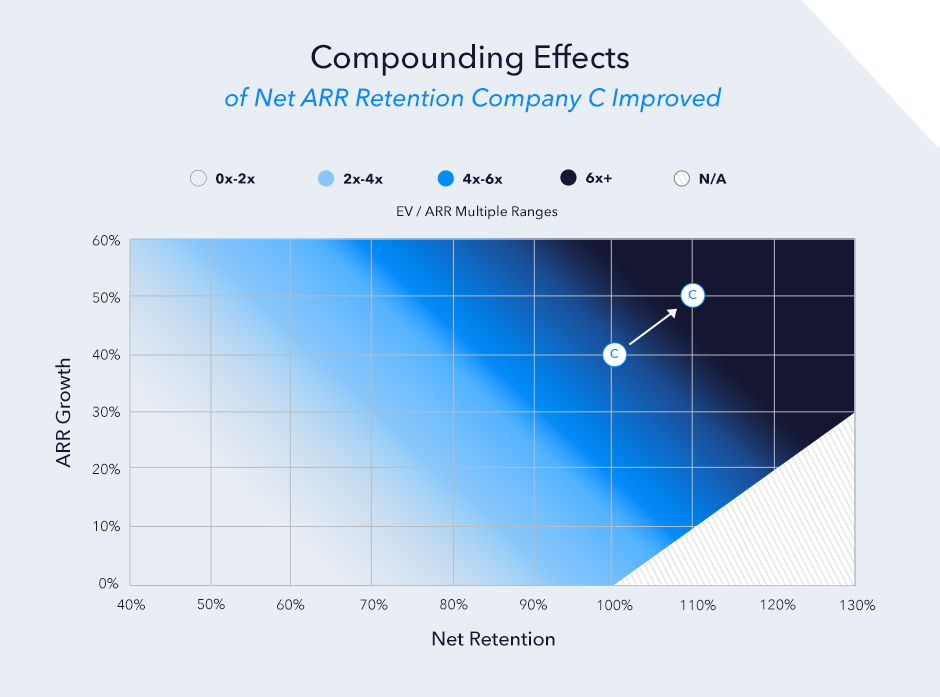

Imagine if Company C improves gross retention from 80% to 90%, all else equal. As a result, Company C will also see net retention improve from 100% to 110%.

Imagine if Company C improves gross retention from 80% to 90%, all else equal. As a result, Company C will also see net retention improve from 100% to 110%.

Because the sales team has not changed its strategy and continues to drive 40% growth, ARR growth increases to 50%. As a result, and similar to compounding interest, the company drives $11.1M more in ARR over a five-year period.

If we are to assume a constant ARR multiple of 7x is applied to both the baseline case and improved retention scenario for Company C, the improved retention scenario has generated $78 million of additional value (EV) over a five year period!

When it comes to valuation and net retention, the company’s size, retention metrics, and growth rate matter. However, the improvements in retention should drive a higher multiple than the base case.

In the example above, it’s not unreasonable to believe Company C’s improved metrics could cause the ARR multiple to expand from 7.0x to 9.0x. In this case, Company C would actually drive $154 million of additional value over five years due to improved net retention!

Retention is within your control today. How much are you focusing on your existing customers? Continuously win over your existing customers, and they will reward the company with a much stronger valuation at capital raise or exit.

One of our SEG clients got it exactly right when they said:

“Having net retention over 100% is like earning compound interest on your customer base every year.”

For most SEG clients serving mid-market to enterprise customers, we see net ARR retention at or above 100%. Don’t hesitate to reach out if you’d like to discuss how retention can impact the valuation for your SaaS company.

Don’t forget to view the full webinar here: How Do You Rank? Understand the Growth and Retention Metrics of SaaS Companies from Recent Surveys and M&A Activity.