Our Services

An overview of our sell-side M&A services

If you’re selling your software business, it’s important to understand key financial variables that may impact the process. One such metric is net working capital (NWC). But when it comes to mergers and acquisitions, calculating NWC and determining a normalized level for the business can be much more nuanced than it appears on the surface.

You might be surprised to find that prospective buyers have their own interpretation of what constitutes NWC. And there may be intense negotiations concerning this number that could delay the closing or impact how much you ultimately take away from the deal. For that reason, it can pay to learn more about NWC, what it might or might not include, and how an M&A advisor can help you negotiate more favorable terms to maximize your proceeds.

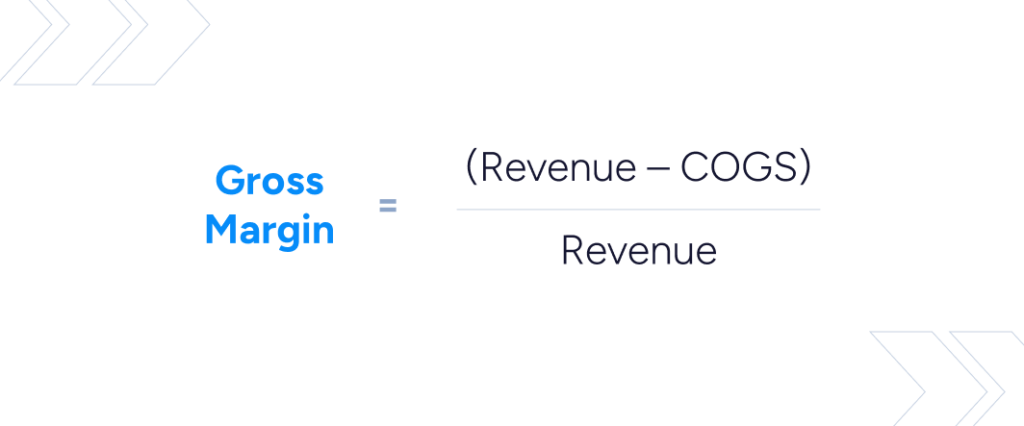

NWC is a fundamental accounting indicator for any business. By its simplest definition, NWC measures the short-term financial health of a business, or its ability to fulfill its near-term obligations. The basic formula takes into account current assets and current liabilities:

Net working capital plays a central role in running your business on a daily basis because it tells you how much capital you have available (or could have in the near term) to cover the company’s near-term obligations. While there are exceptions to every rule, a positive NWC is generally a sign of a healthy business, while a net-zero or negative NWC may indicate the company is at risk of not meeting its obligations.

Negotiating the target and actual NWC amounts is where some acquisition deals get stuck because it seems everyone has a different idea of how to calculate NWC.

First, it’s important to understand that most M&A transactions are completed on a cash-free, debt-free (CFDF) basis. This means the seller keeps all cash remaining on their balance sheet at closing time and must pay off all long-term or interest-bearing debt. The deal is simpler this way, as the purchase price is based solely on enterprise value.

Thus, in a cash-free, debt-free transaction, the standard calculation to find NWC is:

Net Working Capital (NWC) = Current Assets (less cash) – Current Liabilities (less debt)

While NWC is certainly important for everyday operations, it will also play a significant role in the sale of your business. Naturally, any prospective buyer, whether a larger technology company or a private equity firm, will want to fully understand the financial health of the business they’re acquiring. They will want to ensure the business has enough working capital to continue operating successfully on its own well after the acquisition closes.

“At closing time, any difference between the targeted NWC and the actual NWC could result in a dollar-for-dollar adjustment to the purchase price. As a seller, it directly impacts your proceeds from the sale.”

In other words, buyers don’t want to write one check for the acquisition itself, and then immediately have to write another check to keep the business afloat.

As part of the acquisition process, you (the seller) and the buyer will need to agree on a target NWC, which is typically included in the buyer’s letter of intent (LOI). This agreement helps assure the buyer that the acquired business will be in a healthy financial position to carry on when they take ownership.

The target NWC is typically based on a “normalized” level of working capital. While the calculation may seem straightforward, things get more complicated when all parties involved start questioning what exactly should be counted as cash, debt, assets, and liabilities. These accounting intricacies, as it turns out, are open to negotiation. Also, what constitutes “normal” is different in every situation and, as with any business deal, each side will attempt to define the terms in their best interests. While a three-, six-, nine-, or 12-month historical average is often used in SaaS to estimate the ongoing needs of a business, some buyers will attempt to define it as an amount equal to a certain number of months’ operating expenses, or say it should be equal to zero altogether.

If your business is affected by seasonal highs and lows in revenue and/or expenses, analyzing a longer time period might present a more accurate average. Alternatively, examining a shorter timeframe may be more appropriate if your business trajectory has changed dramatically (such as experiencing rapid growth) in the months leading up to the deal closing. Identifying trends on an account-by-account basis is a crucial component of understanding the net working capital profile of a business.

There are also a handful of issues that can arise related to the treatment of specific accounts. For example, deciding how to account for deferred revenue is a common sticking point. In our view, short-term (12 months or less) deferred revenue – that is, the money you’ve collected in advance of delivering the product/service – should always be included in NWC, but buyers will sometimes try to treat this as a debt-like item. Another example is payroll liabilities. Regular payroll expenses should always be included as a liability in the NWC equation. However, accrued bonuses owed to employees should be treated as debt, as these were discretionary decisions made by the seller’s management before the change of ownership.

In any case, the target number should always take into account factors that are most relevant and applicable to the business as it exists today, and taking a proactive approach by calculating/analyzing NWC ahead of time with your banker and accounting advisor will put you in a strong negotiating position when the time comes in your M&A process.

Arriving at a fair target NWC is critical because it could ultimately affect how much you make from the sale. If the NWC left in the business at closing is less than the target, the buyer will expect to be compensated for that. Conversely, if the closing NWC is more than the target, the purchase price will increase.

As the deal closes, your company (the seller) will make an estimate of NWC at the time of closing. Then there will be a “truing up” period (typically 60-90 days) in which adjustments may be made to the sale price based on the actual state of the business once all accounting is complete. Any difference between the actual NWC and estimated NWC at the close is compensated for via the NWC escrow, a small amount of cash held back from the purchase price at close to settle any final minor adjustments. Whatever is left is distributed to the selling shareholders at the end of the true-up period.

| Negotiated NWC Target | $500,000 | Negotiated amount of NWC to remain in business at close |

| Estimated NWC at Close | $600,000 | Estimated at close by Seller |

| NWC Adjustment | $100,000 | Added to initial purchase price at closing |

| Actual NWC at Close (at true-up) | $590,000 | $10K paid out from seller’s NWC escrow to buyer since Actual NWC was $10K lower than Estimated NWC. The remainder of the escrow is then distributed to the shareholders. |

In some transactions, the deal may include a “collar,” which allows for some flexibility in the NWC target so the burden of making minor adjustments can be avoided at closing time. For example, if the final NWC at closing time falls anywhere within the negotiated collar range, no adjustments will be made.

Reaching an agreement on your business’ Net Working Capital is critical to ensuring a fair result for both the buyer and seller. Yet with so many nuances to consider, working with an advisor to manage this key negotiation can help minimize changes in the final purchase price and create a smoother process overall.

For over 30 years, Software Equity Group has provided unparalleled software M&A advisory services for emerging and established software companies. If you’re preparing to sell your business, don’t hesitate to reach out. The experts at SEG can guide you through the factors that matter most to improving the value of your company.