Our Services

An overview of our sell-side M&A services

…one-third of all software/SaaS M&A transactions with ascertainable exit multiples had an EV/Revenue multiple of 3.0x or greater.

This excerpt is from our complimentary Q3 2012 Software Industry Financial Report which can be downloaded here: https://softwareequity.com/research_reports.aspx

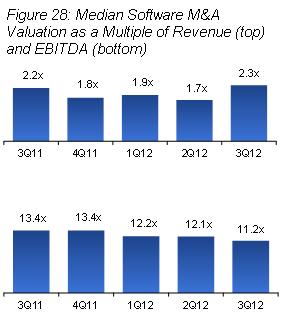

The software industry’s median exit multiple was 2.3x TTM revenue in 3Q12, up sharply from 1.7x in 2Q12 (Figure 28). The 2.3x benchmark is the highest since 2Q11’s 2.5x median exit multiple. It’s worth noting that in Q3, one-third of all software/SaaS M&A transactions with ascertainable exit multiples had an EV/Revenue multiple of 3.0x or greater (Figure 29), and 8.0% of these deals boasted exit valuations of 5.0x TTM revenue or greater.

Among Q3’s transactions with the highest exit multiples were Salesforce.com’s acquisition of GoInstant ($70 million EV, 15.0x TTM revenue estimate); KEYW Holding Corporation’s acquisition of Sensage ($84.8, 7.0x); and SeaEnergy’s acquisition of Return to Scene ($16 million, 5.1x).

The largest SaaS deal of the quarter was IBM’s acquisition of Kenexa, a leading provider of talent management solutions ($1.3B EV, 4.1x TTM Revenue). The deal follows on the heels of acquisitions by SAP and Oracle of Kenexa rivals SuccessFactors and Taleo.

Since very few software transactions publicly disclose a private software seller’s TTM EBITDA, we lacked sufficient data to ascertain the median EBITDA exit multiple paid in 3Q12 for private software company sellers (Figure 28). We did, however, determine 3Q12’s median exit multiple for public software company sellers was 11.2x TTM EBITDA, a modest decline from 2Q12’s 12.1x TTM EBITDA exit multiple.